%201.avif)

7 Must-Have Features for Modern Loan Origination Software

Modern lending moves at the speed of clicks, not paperwork. Borrowers expect instant decisions, while lenders juggle tighter regulations, rising defaults, and mounting competition from fintechs.

That’s where Loan Origination Software (LOS) becomes more than just a workflow tool — it’s the digital command center of lending operations. But not every LOS is built equally.

In our previous guide on Loan Origination Software, we unpacked what LOS is and how it transforms the lending journey. In this blog, we’ll dive deeper into the seven must-have features that separate good LOS platforms from game-changing ones — the features that drive faster approvals, cleaner compliance, and scalable growth.

1. Unified Borrower Experience

Borrowers don’t think in “channels” — they think in experiences. Whether they start an application on a mobile app and finish it on a desktop, the process should feel seamless.

A modern LOS must offer a unified borrower portal with:

- Cross-device continuity (start anywhere, continue anywhere)

- Self-service onboarding (upload KYC docs, eSign forms, check status)

- Embedded communication (chatbots, notifications, and updates)

This omnichannel experience reduces drop-offs, boosts application completion rates, and builds borrower trust. The result? A faster path from interest to approval — with fewer human touchpoints.

2. AI-Powered Credit Decisioning

Speed is nothing without precision. AI-driven credit decisioning helps lenders process more applications without increasing risk.

Using machine learning models trained on historical data, the system predicts borrower risk, flags anomalies, and enhances traditional credit scoring with behavioral and alternative data.

Key components include:

- Real-time data validation from bureaus and APIs

- Automated scoring and decision rules

- Continuous model learning to refine accuracy

This means approvals that once took hours now take minutes — and underwriting becomes data-driven, not guesswork.

3. Configurable Workflow Automation

No two lenders operate alike — which is why rigid workflows are a deal-breaker. A top-tier LOS must offer configurable automation, letting lenders define custom rules, approval hierarchies, and escalation paths.

Examples include:

- Automated routing based on loan type or risk level

- “Four-eye” checks for large-ticket loans

- SLA-driven alerts for bottleneck tracking

Workflow automation minimizes manual handoffs, eliminates redundant tasks, and ensures every loan follows a consistent, auditable path — a huge win for compliance and speed.

4. Built-in KYC, AML, and Compliance Controls

Compliance isn’t optional — it’s a differentiator. The best LOS platforms are compliance-first by design, not by afterthought.

That means:

- Native integration with KYC/AML APIs (Aadhaar, CKYC, Plaid, Onfido, etc.)

- Automated document verification with OCR

- Audit-ready logs that track every step and decision

Global lenders must also meet frameworks like GDPR, SOC 2, ISO 27001, and local financial conduct standards. Embedding these into your LOS ensures real-time risk monitoring and effortless audit readiness — without slowing down operations.

5. Seamless API Integrations

An LOS doesn’t live in isolation — it’s the connective tissue of your lending tech stack. Modern systems come with open APIs and pre-built integrations that plug into your existing ecosystem:

- Core banking systems

- Credit bureaus and risk data providers

- CRMs like HubSpot or Salesforce

- Payment gateways and eNACH systems

- Loan Management Systems (LMS) for post-disbursal operations

With APIs doing the heavy lifting, lenders gain a single source of truth across the borrower lifecycle. This integration-driven approach also future-proofs your tech stack, letting you adopt new modules without ripping out the old ones.

6. Real-Time Analytics & Reporting Dashboards

Every decision in lending carries risk — but the smartest lenders use real-time analytics to stay ahead of it.

Advanced LOS platforms come equipped with custom dashboards and visual analytics that track:

- Application turnaround time (TAT)

- Default probability by segment

- Approval rates and rejection reasons

- Team performance and SLA compliance

This insight helps teams identify patterns, measure ROI, and continuously optimize operations. It turns LOS from a passive tool into an active decision partner.

7. Scalable, Secure Cloud Architecture

Global lenders operate across geographies, regulations, and time zones. To handle that complexity, an LOS must be cloud-native and enterprise-secure.

Look for:

- Multi-tenant cloud deployment (AWS, Azure, or GCP)

- Role-based access control and encryption-at-rest

- High uptime and disaster recovery support

- Compliance with SOC 2, ISO 27001, and GDPR standards

Cloud-based LOS platforms also scale on demand — letting you handle peak application loads without breaking infrastructure or performance.

In short: security and scalability aren’t “features.” They’re the foundation.

Why These Features Matter

These seven features don’t just add convenience — they directly impact your bottom line:

- Faster decisions → higher conversion rates

- Automated compliance → lower risk and audit costs

- Unified experiences → happier borrowers and better retention

Together, they transform LOS from a processing system into a growth engine for modern lending institutions.

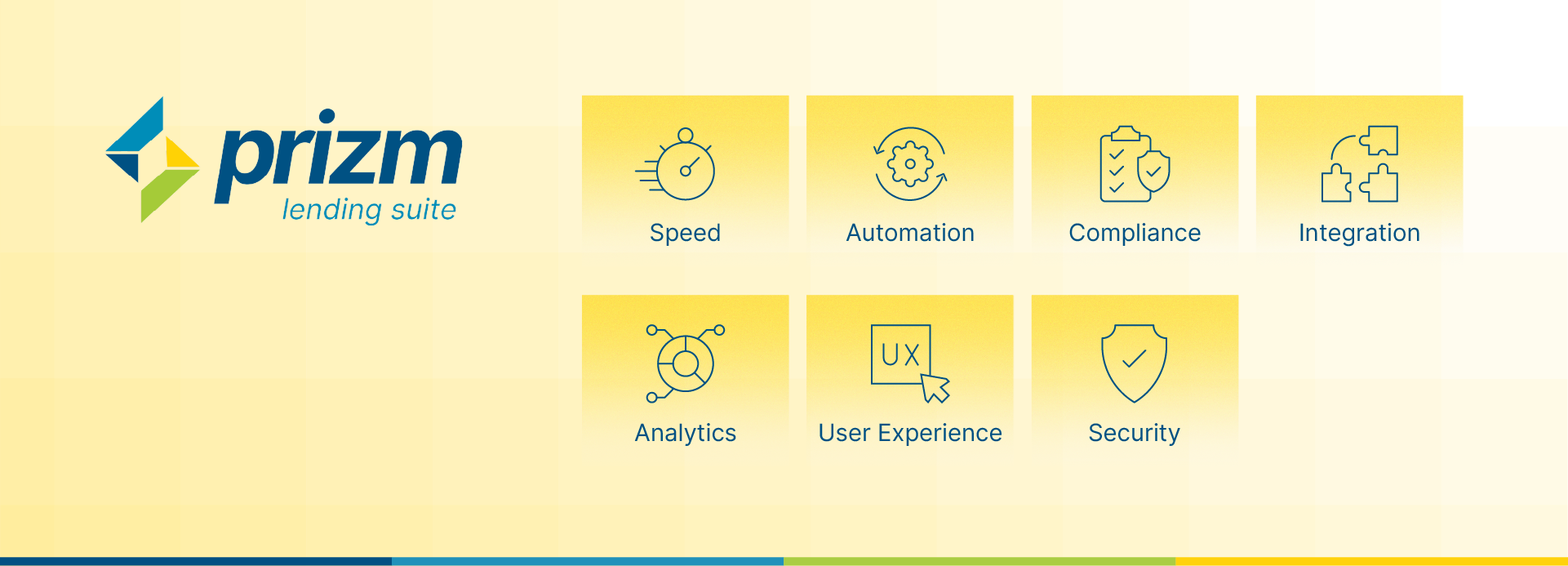

It’s Time to Modernize Your LOS?

If your current system still relies on spreadsheets, emails, or rigid workflows, it’s time for an upgrade. Finspectra PRIZM LOS brings all these capabilities into one intelligent platform — blending automation, compliance, and analytics to help lenders move faster and lend smarter.

Book a demo to see how PRIZM LOS can streamline your lending operations from application to disbursal.

FAQs

1. How does loan origination software improve approval times?

By automating tasks like KYC, document checks, and scoring, LOS reduces manual touchpoints and speeds up decision-making — turning hours into minutes.

2. Can loan origination software reduce errors in loan processing?

Yes. Automation minimizes data re-entry, enforces rule-based validation, and maintains complete audit trails for accuracy and accountability.

3. What should lenders look for when choosing loan origination software?

Look for configurable workflows, compliance-ready architecture, API flexibility, and robust analytics. A great LOS should adapt to your business, not the other way around.

4. How do I evaluate a loan origination software vendor’s security and compliance?

Ensure they meet global standards like ISO 27001, SOC 2, and GDPR, and provide clear documentation on encryption, data governance, and role-based access.

5. What are the steps to migrate from legacy lending software to a cloud-based LOS?

Start with data cleanup, define workflows, run pilot testing, and choose a phased rollout. Modern vendors often provide migration support to minimize downtime.

.png)

.png)

.png)