%201.avif)

How Unified Customer Profiles Improve Loan Underwriting and Collections

Consider this scenario: A long-standing customer applies for a business loan. The underwriting team sees a borderline credit score and declines the application. Meanwhile, the deposit side of the bank knows this same customer holds substantial balances and has never overdrawn.

Flip the coin: A borrower misses a payment. Collections immediately initiates aggressive outreach. They don't realize this borrower is currently negotiating a loan modification with another department or has a pending service complaint already logged.

This isn't a system failure. It's what happens when your left hand doesn't know what your right hand is doing.

The fragmentation of customer data doesn't just slow operations; it creates blind spots that lead to bad credit decisions, missed collection opportunities, and borrowers who feel like strangers every time they interact with you.

A unified customer profile brings all data under a single roof to transform underwriting, risk assessment, collections, and entire lending workflows.

What Is a Unified Customer Profile?

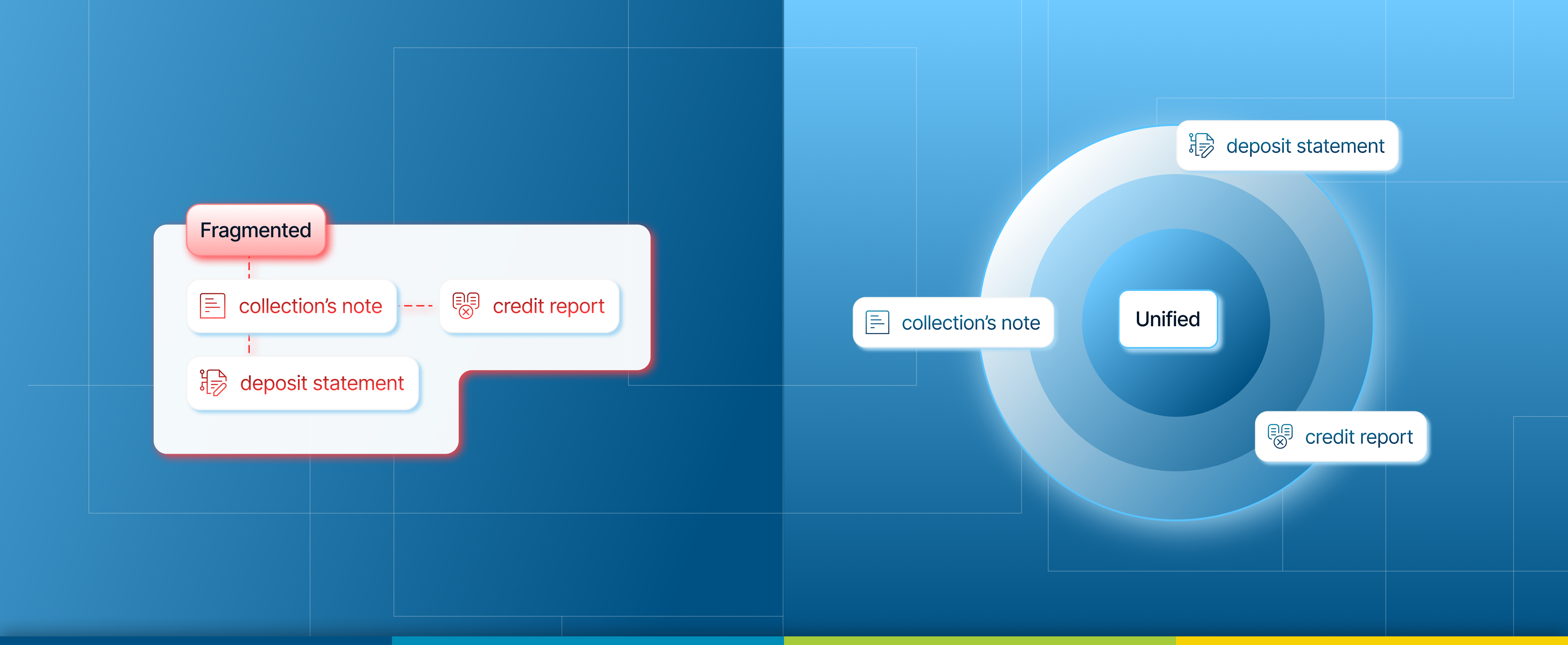

A unified customer profile is the "Golden Record": a single, real-time source of truth that aggregates every borrower interaction across all systems. Credit history, transaction behavior, communication logs, payment patterns, collateral details, and real-time account status.

Not a copy. Not a summary. A live, connected record.

Traditional lending systems store customer data in silos: loan origination here, servicing there, collections somewhere else. Each system has its own version of the truth. When an underwriter needs the full picture, they're stitching together fragments. When a collections agent calls, they're flying blind on recent payment attempts or disputes already logged.

A unified profile eliminates that archaeology. One borrower. One record. Updated in real time across every touchpoint.

Why Fragmented Data Breaks Underwriting and Collections

The Underwriting Problem:

Underwriters make risk decisions based on incomplete information. They pull credit scores, income statements, and existing obligations, but miss critical context. Did this borrower recently refinance with you? Are they current on three other products but delinquent on one? What do their deposit trends reveal about financial health?

Without unified data, underwriters either over-rely on external credit scores or waste hours manually reconciling internal records. The result? Slower decisions, inconsistent risk assessment, and missed opportunities to approve good borrowers or flag bad ones early.

A borrower with a 680 score might look marginal in isolation. But if unified data shows declining deposit trends before the loan is even booked, that's predictive intelligence that traditional underwriting misses entirely.

The Collections Problem:

Collections teams operate in a reactive mode. By the time an account hits their queue, they're working from a snapshot: days past due, outstanding balance, last payment date. What they don't see: the borrower's full relationship with the lender, recent disputes, hardship requests already submitted, or payment plans offered by another department.

This leads to redundant outreach, contradictory messaging, and borrowers who disengage entirely because "you people don't talk to each other."

How Unified Profiles Transform Credit Risk Assessment

Complete Risk Context:

Unified profiles give underwriters the full borrower story. Not just credit score and DTI ratio, but payment consistency across products, response patterns to past communications, and behavioral signals that predict default risk better than static snapshots.

If a borrower has been current on two loans with you for three years and always responds to reminders within 24 hours, that's actionable intelligence. Unified profiles surface it instantly.

- Automated Underwriting with Better Data: Automated loan underwriting works when the data feeding it is clean and complete. Unified profiles eliminate the manual verification loops that slow approvals. Systems can pull real-time account status, cross-reference existing obligations, and flag inconsistencies without human intervention. The result: faster decisioning, fewer exceptions, and risk models that actually reflect borrower behavior instead of guessing at it.

- The Feedback Loop: Here's the best part: insights flow both ways. Data gathered during collections like, reasons for non-payment, successful recovery strategies, feeds back into underwriting models. Today's collection experience refines tomorrow's credit decisions. This continuous intelligence loop makes your risk assessment smarter over time.

- Delinquency Management That Sees Around Corners: Collections teams don't need to wait for accounts to go delinquent. Unified profiles track early warning signals: missed autopay setups, declining transaction activity, communication drop-offs. Collections analytics can prioritize outreach before accounts spiral.

Collections prioritization becomes surgical with a unified customer profile:

The Forgetful Payer: High-net-worth client who missed due to travel, send a gentle digital nudge.

The High-Risk Debtor: Declining deposits, maxed credit lines: immediate intervention required.

An agent calling a 30-day delinquent account sees everything: recent loan modifications, hardship documentation, preferred contact methods, and whether this borrower typically self-cures or needs intervention. That context changes the conversation from adversarial to supportive.

The Hidden Cost of Scattered Customer Data

Scattered data impacts operational efficiency:

- Operational Drag: Staff spend hours reconciling records, verifying data accuracy, and explaining to borrowers why "the system" doesn't reflect their last payment. Every fragmented interaction multiplies effort.

- Risk Exposure: Incomplete data leads to bad credit decisions—approving risky loans or rejecting good ones. It also exposes lenders to compliance risk when auditors ask for complete borrower documentation and you're pulling from six sources.

- Customer Friction: Borrowers notice when you don't know them. Asking for information already provided. Contradicting statements made by another department. Treating a long-term customer like a stranger. That friction drives attrition.

What to Look For in a Unified Customer Data Platform

A unified customer data platform improves credit decisions and collections efficiency. It gives all the information about customer on a single interface. It enables:

- Real-Time Synchronization: Data updates should flow instantly across systems. A payment processed in servicing should appear in collections views immediately—not after nightly batch updates.

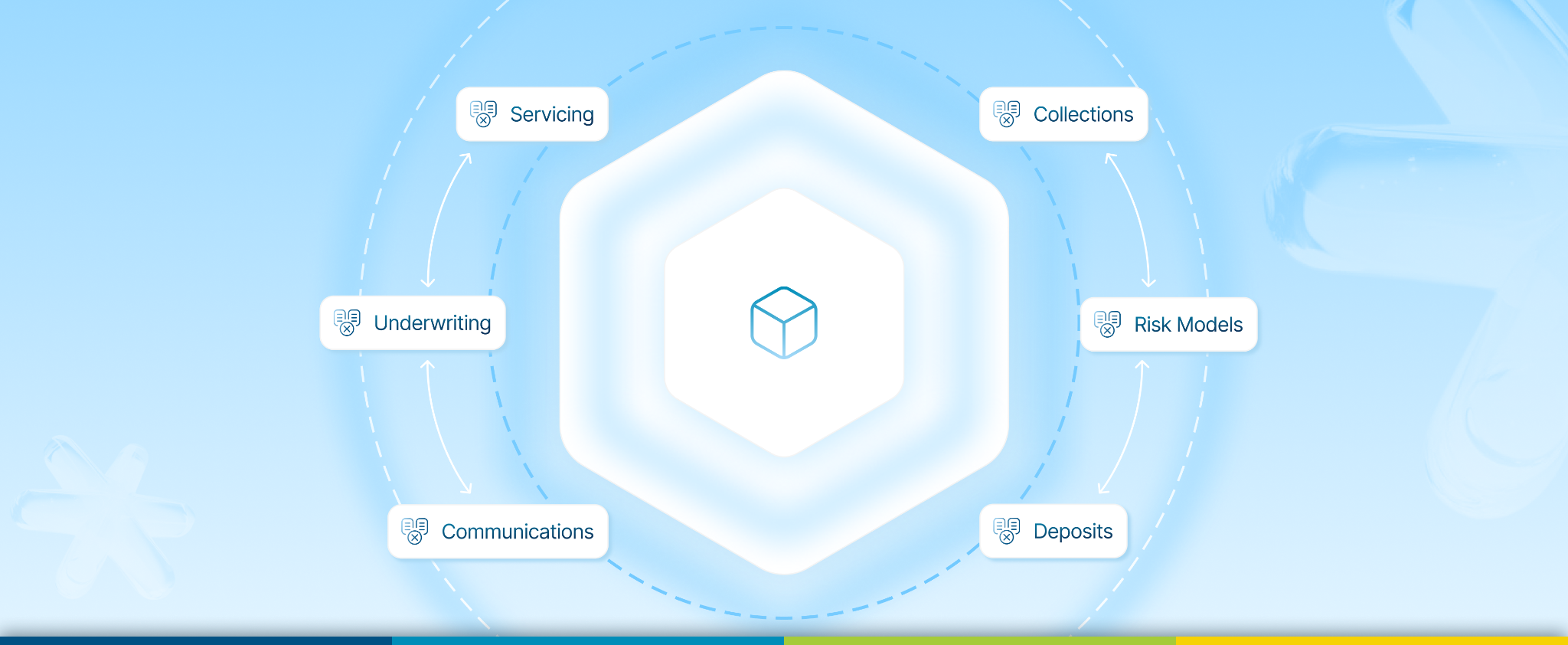

- Cross-Product Visibility: Lenders managing multiple products need profiles that show the complete relationship: mortgages, personal loans, lines of credit. Risk assessment improves when underwriters see portfolio-level behavior, not isolated accounts.

- Embedded Analytics: Unified profiles are only valuable if insights are actionable. Look for platforms that surface risk scores, delinquency predictions, and collection prioritization natively, not as separate reporting tools.

- Audit Trail Integrity: Every data point should be traceable: where it came from, when it changed, who accessed it. This protects lenders during audits and disputes.

The Strategic Bridge

The divide between underwriting and collections is artificial. They're two sides of the same coin. Unified profiles eliminate this false boundary. You stop treating customers as "Application #1234" in underwriting and "Case File #9876" in collections.

Unified profiles aren't just operational upgrades. They're strategic infrastructure, the foundation for agile risk management, regulatory compliance, and customer-centric innovation. Lenders who operate with fragmented data will suffer higher defaults and lower retention. Those who unify will build resilient, profitable portfolios.

This is where Finspectra's Prizm Lending Suite stands out: it unifies customer data across origination, servicing, and collections into a single Golden Record that updates in real time. Underwriters and collections agents work from the same truth, enabling faster decisions and smarter strategies.

Ready to see how unified profiles transform underwriting and collections? Book a Prizm demo today!

FAQs

- What is a unified customer profile in lending?

A unified customer profile consolidates borrower information from multiple channels into one authoritative view, enabling seamless access across lending teams without data duplication or delays.

- How does unified customer data improve credit underwriting?

It delivers holistic borrower insights that sharpen risk models, accelerate approvals for qualified applicants, and flag subtle patterns traditional scores overlook.

- Can unified profiles help reduce loan defaults?

Unified profiles enable predictive monitoring that identifies at-risk accounts early, triggering timely adjustments before delinquencies escalate.

- What data sources are used to create a customer 360 view?

Core sources span transaction histories, interaction logs, external validations, and portfolio records, fused into a dynamic, query-ready profile.

- How does unified borrower data improve collections efficiency?

Agents gain instant visibility into relationship history, streamlining outreach sequencing and tailoring recovery tactics for higher success rates.

.png)

.png)

.png)