%201.avif)

How to Accelerate Loan Disbursement Without Increasing Risk Exposure

Speed and caution have always existed in tension inside lending institutions. Ask any credit risk officer and they will tell you the same thing: the fastest way to disburse a loan is also, historically, the fastest way to accumulate bad debt. And yet, in a market where borrowers comparison-shop across three lenders before breakfast, the institutions that cannot close quickly are already losing.

The question is not whether to move faster. The question is how to do it without dismantling the controls that keep a portfolio healthy. This blog examines the structural, technological, and process-level levers that allow lenders to compress loan processing time without trading away underwriting discipline.

Why Speed Has Become a Competitive Necessity

The expectation gap in lending has widened considerably over the last decade. Consumer borrowers now expect decisions in minutes, not days. Small business owners, who need working capital to meet payroll or capture a procurement opportunity, cannot wait two weeks for a credit committee. Even mortgage applicants, who have traditionally tolerated long timelines, are increasingly walking away from lenders that cannot give them certainty within 48 to 72 hours.

This pressure is not imaginary, and it is not limited to retail lending. Corporate treasurers evaluating term loan facilities factor in process speed as a proxy for relationship quality. If a bank cannot run its own internal approval machinery efficiently, clients reasonably wonder what that says about how the institution manages everything else.

If your approval timelines are still measured in days, the root causes are worth examining carefully. Check this blog: why loan approvals still take days and what lenders can do differently.

At the same time, the risk landscape has become more complex. Macroeconomic volatility, thin fraud detection windows, and regulatory scrutiny around fair lending practices mean that lenders cannot simply strip out verification steps to gain velocity. The answer has to be smarter, not blunter.

What the Loan Disbursement Process Actually Looks Like Under the Hood

Before discussing how to accelerate, it helps to be precise about what is actually being accelerated. The loan disbursement process is not a single step. It is a sequence, and the inefficiencies are distributed unevenly across it.

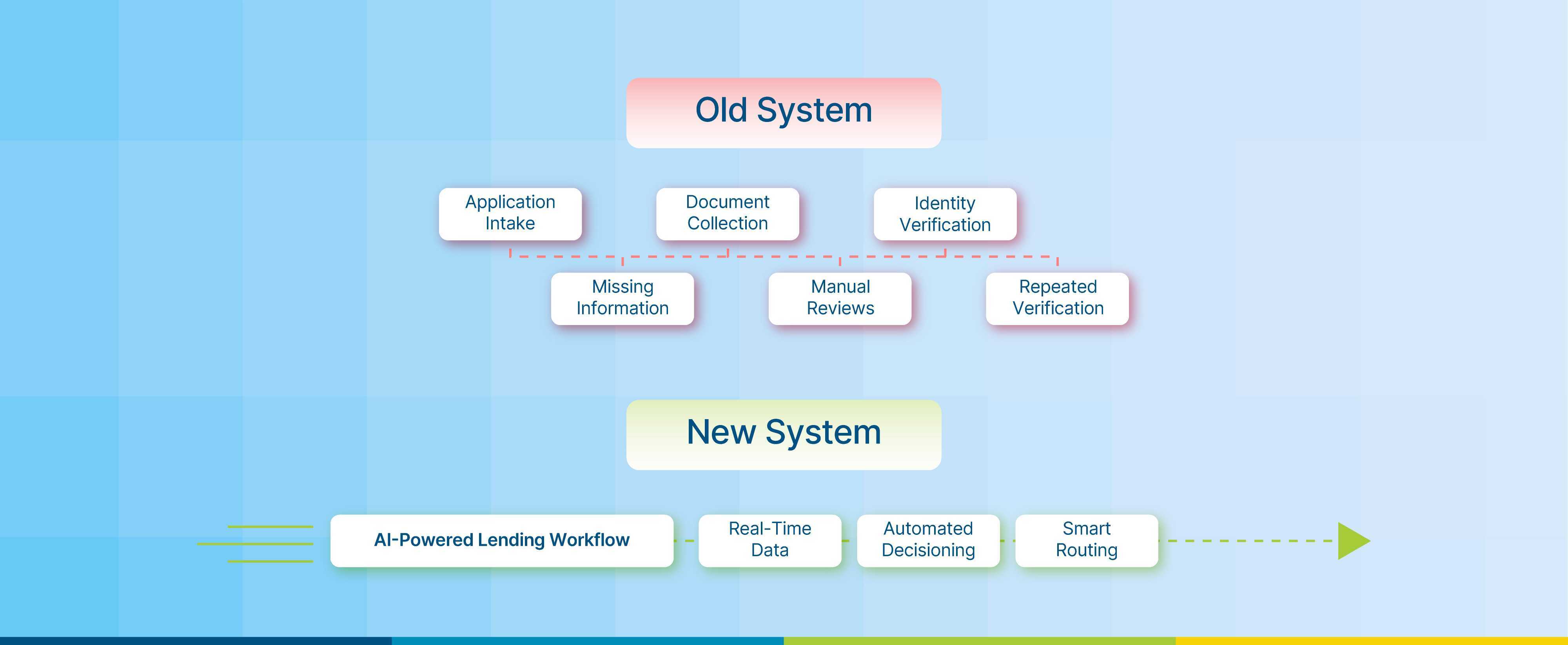

At a structural level, the process typically moves through these stages: origination and application intake, document collection and verification, creditworthiness assessment, approval decision, documentation execution, and finally, fund transfer. Each of these stages carries its own failure mode.

Origination suffers from incomplete data capture. Borrowers submit forms with missing fields, contradictory information, or documents that do not match the application. Every gap creates a re-touch cycle.

Verification is often the single largest time sink. Lenders that rely on manual review of bank statements, payslips, or identity documents are operating with a 2010-era toolkit in a 2025 market. A single verification queue can hold applications for three to five business days.

Credit assessment slows down when analysts are working from static, backward-looking data. Traditional bureau scores reflect credit history up to 90 days prior. By the time a decision is made on that information, the borrower's financial position may have shifted materially.

Documentation execution still involves wet signatures and courier logistics at many mid-tier lenders, adding 24 to 72 hours after approval.

Fund transfer is often the most reliable step, but it is contingent on everything upstream completing without error.

Understanding this topology matters because different bottlenecks require different interventions. Buying a faster core banking system does not fix a broken document collection workflow.

The Role of Automation in Compressing Loan Processing Time

Automated loan processing is not a uniform concept. The term covers a range of capabilities, from simple rule-based decisioning engines to sophisticated machine learning models that synthesize hundreds of data signals simultaneously. What matters is matching the right automation to the right bottleneck.

Intelligent Document Processing

The most immediate return on automation investment typically comes from document handling. Intelligent document processing systems can extract data from uploaded bank statements, identity documents, and financial filings in seconds, validate them against application data, and flag discrepancies before a human ever touches the file. Lenders who have deployed these systems report a 60 to 80 percent reduction in manual document review time. More importantly, they are catching errors earlier, which prevents downstream rework that is far more expensive.

For a deeper look at how origination-stage automation specifically reduces turnaround time, see how intelligent loan origination software cuts TAT and eliminates processing delays.

Rules-Based and AI-Augmented Decisioning

Automated decisioning has matured considerably. Modern credit engines can process hundreds of loan approval process steps in parallel: income verification, debt-to-income calculation, fraud pattern detection, policy eligibility checks, and bureau pulls. For standardized products like personal loans, auto loans, or small-ticket MSME loans, a significant percentage of applications can reach a decision entirely within the automated pathway without requiring analyst intervention. This is not about removing human judgment. It is about reserving human judgment for cases where it actually adds value.

API-Led Data Integration

One of the quieter revolutions in lending operations is the shift toward real-time data via APIs. Account aggregation platforms can now surface live transaction histories with borrower consent. GST data, ITR filings, and payroll data can be pulled directly from source systems rather than waiting for the borrower to upload documents. This compresses the data collection phase from days to seconds while simultaneously improving data quality, because the data comes directly from authoritative sources rather than borrower-supplied documents that may be altered or outdated.

Risk Controls That Enable Speed Rather Than Impede It

Here is the counterintuitive truth about risk management in modern lending: well-designed controls actually accelerate the loan disbursement process by eliminating uncertainty. The problem with legacy risk frameworks is not that they are rigorous. It is that they are slow because they are manual and sequential.

Fraud signals that once required a back-office analyst to identify are now detectable in milliseconds using behavioral analytics and device intelligence. The stakes of getting this wrong are not abstract: Alloy's 2024 State of Fraud Benchmark Report, which surveyed 450 fraud decision-makers across US and UK financial institutions, found that over 57% of organizations absorbed more than $500,000 in direct fraud losses in a single year, with one in four losing over $1 million.

Real-Time Fraud Detection

Fraud signals that once required a back-office analyst to identify are now detectable in milliseconds using behavioral analytics and device intelligence. A fraudulent application that would have passed through a manual workflow and been flagged only at disbursement can now be caught at origination. This protects the portfolio and removes a category of exception cases that clog approval queues.

Dynamic Credit Decisioning

Static scorecards give every borrower who falls within a band the same treatment. Dynamic models can identify within-band variance, segmenting borrowers who represent lower actual risk from those who represent higher risk. This creates space to offer expedited processing to strong-profile applicants while routing complex or borderline cases to more intensive review, without treating every application as if it requires the same level of scrutiny.

The gap between old and new here is significant: McKinsey's 2024 analysis found that AI-driven credit models assess up to 10,000 data points per borrower, compared to 50 to 100 in traditional scoring.

Exception Management Architecture

One of the most underrated levers in lending process optimization is designing the exception pathway explicitly. Many lenders have clear processes for standard cases but poorly defined processes for exceptions. When an anomaly surfaces, an application goes into a vague "needs review" bucket where it sits until someone has bandwidth. A structured exception framework assigns exception types to specific resolution pathways, sets SLAs for resolution, and routes alerts to the right analyst. The result is that exceptions get resolved faster without creating audit risk.

The Organizational Dimension of Processing Speed

Technology accounts for a significant share of speed gains, but it does not account for all of them. Lenders that have invested in automation but still face extended loan processing time often discover that the remaining drag is organizational.

Handoff latency is a common culprit. Even when individual tasks complete quickly, delays accumulate at the boundaries between teams: between sales and credit, between credit and legal, between legal and operations. Mapping these handoffs explicitly and setting inter-department SLAs is unglamorous work, but it regularly surfaces days of latency that no software can fix.

Approval authority structures also matter. In institutions where a senior credit officer must sign off on every loan above a relatively low threshold, the committee process becomes a bottleneck. Rationalizing approval authority, including delegated authority frameworks that allow relationship managers or branch heads to approve certain loan categories up to defined limits, can significantly reduce decision cycle time without expanding credit risk.

Feedback loops between origination and underwriting teams help improve application quality over time. If underwriters are consistently receiving incomplete applications from a particular channel or product, that insight needs to reach the people configuring those intake flows. Without structured feedback, the same errors repeat indefinitely.

How to Balance Speed and Risk: A Framework

The tension between velocity and caution resolves more cleanly when lenders move from a binary "approve / decline" mindset to a risk-tiered processing model.

The simplest version of this framework has three lanes:

Green lane for applications that meet all policy criteria with high confidence scores across income, identity, bureau, and fraud signals. These applications move through automated loan processing end to end. Human involvement is minimal, and disbursement can happen within hours of application completion.

Yellow lane for applications that meet basic criteria but carry one or more signals that warrant review, whether a thin credit file, a data mismatch, or an income source that requires additional documentation. These applications move faster than a fully manual process but involve targeted analyst review of the specific issue, not a full re-underwrite.

Red lane for applications that trigger hard policy rules or significant fraud signals. These are declined or referred, with documentation that satisfies regulatory requirements around adverse action.

This model is not novel in concept, but relatively few lenders have operationalized it rigorously. Many still route all applications through a single pipeline, which means the complexity of borderline cases slows down the processing of clean cases.

Building this kind of tiered architecture end-to-end requires more than a decisioning engine and it requires the full workflow to be designed around it. The complete guide to creating a fully automated lending workflow covers how that infrastructure comes together.

Measuring What Actually Matters

Lending process optimization efforts often fail to produce durable results because institutions measure activity instead of outcomes. Application volumes, documents uploaded, and committee meetings held are activity metrics. What matters is cycle time by stage, with a breakout showing where time is actually accumulating.

Useful metrics for a speed-and-risk balanced operation include:

- Time from complete application to credit decision, segmented by product and channel

- Rework rate: the percentage of applications that require additional information requests after initial submission

- Exception rate by category: what types of exceptions are most common, and how long they take to resolve

- Decision accuracy over time: whether faster decisions are producing higher early delinquency rates, which would indicate that speed gains are coming at the expense of underwriting quality

Tracking these metrics consistently, and connecting them to specific process interventions, is what separates sustainable optimization from one-time speed initiatives that erode over time.

FAQs

What is the loan disbursement process?

The loan disbursement process refers to the full sequence of steps from loan application through fund transfer. This includes application intake, document collection, identity and income verification, credit assessment, approval decision, loan agreement execution, and the actual release of funds to the borrower. Each stage has its own timelines, stakeholders, and failure modes.

How can lenders reduce loan processing time?

Lenders reduce loan processing time by automating high-volume, low-judgment tasks such as document extraction and initial data validation; using API integrations to source financial data in real time rather than relying on borrower-supplied documents; implementing risk-tiered processing that routes clean applications through faster pathways; and rationalizing internal handoffs and approval authority structures.

What causes delays in loan disbursement?

The most common causes are incomplete applications at origination, manual document review queues, sequential rather than parallel processing of verification tasks, poorly defined exception management pathways, and legacy approval structures that require senior committee sign-off on routine decisions. Organizational handoff latency between departments is also a significant factor that technology alone cannot resolve.

How does automation speed up loan approvals?

Automated loan processing speeds up approvals by executing multiple verification tasks simultaneously rather than sequentially, by eliminating re-touch cycles caused by manual data entry errors, by enabling real-time data retrieval that removes document collection delays, and by allowing clean applications to reach a decision entirely within the automated pathway without human intervention.

How can lenders balance speed and risk in lending?

The most effective approach is a risk-tiered processing model that routes applications into fast, moderate, or intensive review pathways based on their risk signal profile. This allows lenders to offer rapid disbursement to low-risk borrowers while maintaining rigorous review for complex cases. Combining real-time fraud detection, dynamic credit models, and structured exception management creates a framework where speed and control reinforce rather than undermine each other.

.png)

.png)

.png)