%201.avif)

Why Loan Approvals Still Take Days and What Lenders Can Do Differently

A mid-market manufacturer applies for a $500,000 equipment loan on Monday morning. The relationship manager logs the application in the CRM. Underwriting requests tax returns via email. Finance pulls credit reports manually. The credit committee meeting isn't until Thursday. Final approval? Maybe next week, if nobody's on vacation and the borrower submitted everything correctly the first time.

The uncomfortable truth: while 30% of banks can approve small and simple loans within one business day, the majority still take 5-10 business days for typical small business loans. For commercial mortgages and complex deals, 30-45 days is normal. In a market where business borrowers comparison-shop like consumers and competitors promise 48-hour decisions, slow loan approval doesn't just frustrate customers; it costs deals.

Most lenders run on fragmented workflows built for a different era: separate systems for origination, underwriting, and credit decisioning; manual data aggregation across platforms; email-based document collection; and approval processes that require physical sign-offs.

Fixing this requires an understanding of where delays actually happen, why they matter more now than ever, and what modern lenders are doing differently.

Why Loan Approvals Still Take Days

Loan approval speed is determined by how much friction exists between systems, people, and processes. The delays stem from structural problems that compound throughout the lending lifecycle.

Customer information lives in the core banking system. Credit bureau data sits in a separate platform. Financial statements arrive via email. Tax returns get uploaded to a shared drive. Collateral valuations come from third-party vendors. Underwriters waste hours reconciling data across sources before analysis even begins. Small businesses spend many hours filling out applications and submitting paperwork, and lenders spend nearly as long chasing missing documents.

Every handoff between departments creates a delay. Application intake forwards to credit administration. Credit administration requests documents from the borrower. The borrower responds (eventually). Someone manually enters financial data into spreadsheets. Underwriting calculates ratios by hand. The credit memo gets drafted, reviewed, revised, and routed through approval hierarchies via email. Each step adds hours or days.

Most lenders treat loan approvals like assembly lines: complete step one, then move to step two, then step three. Applications sit in queues waiting for the next available resource. Credit committee meetings happen on fixed schedules weekly if you're lucky, biweekly if you're not. Deals that miss the cutoff wait another cycle.

The result? Response times that stretch from 4 to 6 weeks for complex commercial loans, even when underwriters could make decisions in days with the right information at the right time.

Where Delays Actually Happen in the Loan Lifecycle

Delays happen at every stage in the loan lifecycle because one process waits for data from the previous step.

Borrowers submit incomplete applications because paper forms don't validate data in real time. Lenders discover missing information days later during initial review. Email threads with "please provide" requests bounce back and forth. Nobody has visibility into what's outstanding or who's responsible for follow-up. Time lost: 2-5 days.

Underwriters receive financial statements as PDFs. Someone manually keys data into spreadsheets, a process prone to typos and inconsistency. Different analysts spread financials differently, creating approval variability. Credit bureau pulls happen manually, often requiring separate logins and downloads. Time lost: 1-3 days.

Credit memos get written in Word documents, circulated for review via email, and revised through tracked changes. Supporting calculations live in undocumented Excel files. Underwriters wait for credit committee meetings to present deals. Committees review stacks of paper without real-time data or portfolio context. Time lost: 3-7 days.

Once credit approves, operations generates loan documents manually copying terms from the credit memo into templates, calculating payment schedules, and assembling closing packages. Legal review adds another layer. Any errors discovered require restarting portions of the process. Time lost: 2-4 days.

Add it up: 8-19 days of pure operational drag before accounting for borrower delays, missing information, or approval exceptions.

Impact of Slow Loan Approvals on Lenders

Faster loan processing time is a competitive differentiator with quantifiable business impact.

Business borrowers who need equipment financing, working capital, or acquisition funding don't wait weeks for answers. They talk to multiple lenders simultaneously. With only 39% approaching large banks for small business loans, the lenders who respond first often win regardless of rate. Every day of delay increases the probability that borrowers accept competing offers.

Manual processes scale linearly with volume. Adding 100 applications means adding proportional staff hours for document collection, data entry, financial spreading, and credit memo prep. Relationship managers spend more time on administrative coordination than on revenue-generating activities.

When underwriters rush to meet turnaround expectations with manual workflows, quality suffers. Ratio calculations get skipped. Covenant structures vary by analyst. Exception approvals happen based on relationship pressure rather than risk assessment. The portfolio inherits consequences months later when credits deteriorate.

Borrowers expect transparency. "Let me check and get back to you" doesn't cut it when fintech competitors provide real-time application status dashboards. Silence during underwriting feels like indifference. Even approved borrowers remember the friction.

What Modern Borrowers Expect Today

The expectation gap between what borrowers want and what traditional lenders deliver has never been wider.

Business owners run companies using cloud-based accounting software that updates in real time, procurement platforms that approve purchases instantly, and SaaS tools with one-click signup. They've internalized consumer fintech speed: personal loans in 24 hours, credit card approvals in minutes, mortgage pre-approvals in days.

Now they expect the same from commercial lenders, even for complex, relationship-based business loans.

Modern borrowers want:

- Application status visibility without calling their relationship manager

- Document submission through digital portals, not email attachments

- Decision timelines measured in days, not weeks

- Transparent communication about what's missing and why

These aren't unreasonable demands. They're baseline expectations shaped by every other business interaction borrowers have. Lenders who can't meet them get compared unfavorably to competitors who can.

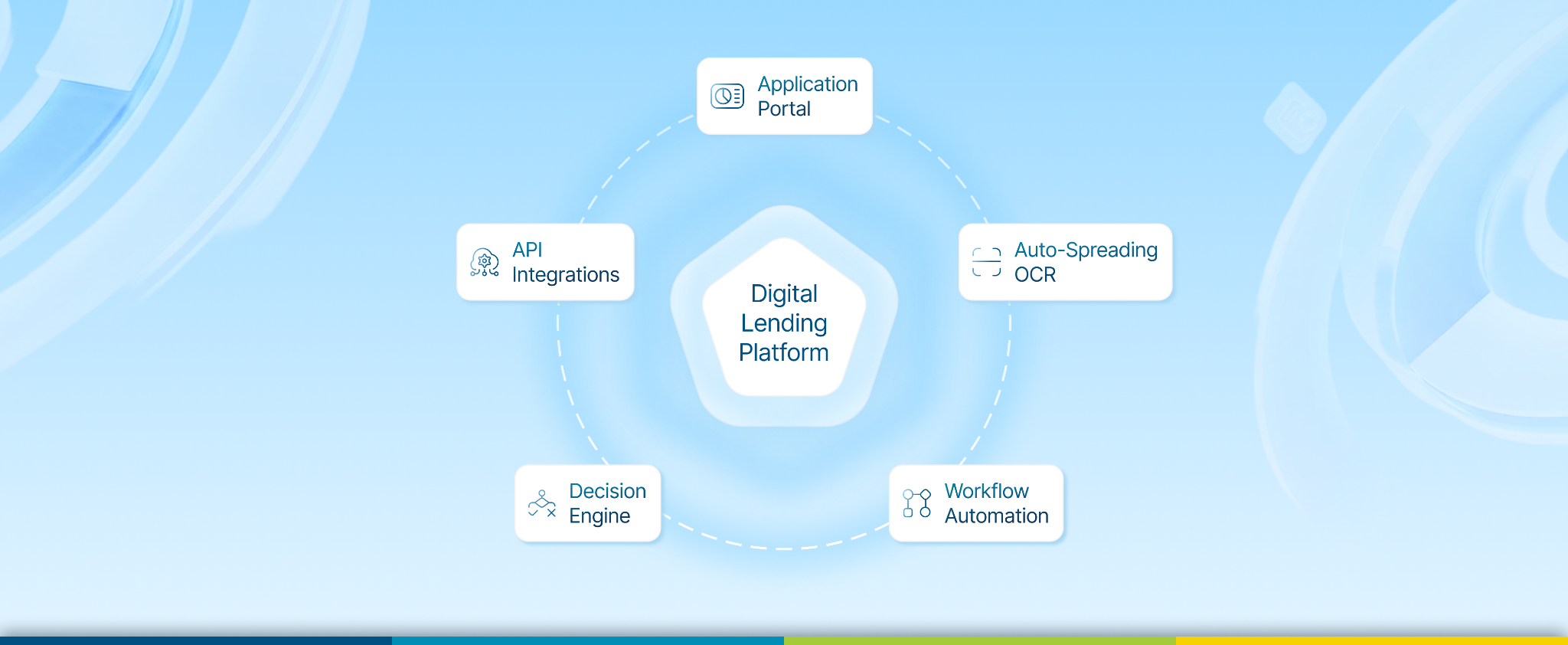

How Digital Lending Changes Approval Timelines

Modern digital lending platforms eliminate entire categories of delay.

All borrower information application data, financial statements, credit reports, collateral valuations, and existing relationship history live in one system. Underwriters see complete credit profiles instantly. No reconciliation. No version control disasters. No spreadsheet archaeology.

OCR technology extracts data from PDFs automatically. Financial spreading happens in seconds instead of hours. Document validation flags missing information at submission, not days later during review. Borrowers upload files to portals that track completion status in real time.

Digital workflows enable simultaneous activities: credit bureau pulls trigger automatically at application; financial analysis runs while collateral gets valued; compliance checks happen during underwriting, not sequentially. Bottlenecks disappear when systems orchestrate tasks intelligently.

Pre-configured credit policies automate routine approvals. Loans that meet standard criteria get instant decisions. Edge cases route to underwriters with pre-analyzed data and exception flags already surfaced. Credit committees focus on truly complex deals, not administrative approval workflows.

The result? Approval timelines that compress from weeks to days, sometimes hours, for standardized products.

For more on how modern lending platforms work end-to-end, explore our loan management system guide.

What Lenders Can Do Differently Today

Faster approvals don't require abandoning relationship-based underwriting or loosening credit standards. They require eliminating operational waste. Here’s what modern lenders can do to speed up loan approval workflow:

- Implement Digital Application Portals: Start accepting loan applications online. Web-based portals validate data at entry, guide borrowers through required documentation, and provide real-time status visibility. Relationship managers stop chasing documents and start advising clients.

- Automate Financial Spreading: OCR and financial spreading engines eliminate manual data entry. Underwriters review analyzed financials in minutes. Standardization reduces approval variability across credit teams.

- Integrate Credit Decisioning Tools: Risk models that pull borrower data automatically, calculate ratios instantly, and surface exceptions immediately give underwriters the context they need to make confident decisions fast. Credit memos become decision summaries, not research projects.

- Enable Workflow Automation: Rule-based routing sends applications to the right underwriter based on loan type, size, and complexity. Approval hierarchies trigger automatically based on authority levels. No more email chains asking "whose queue is this in?"

- Connect Systems via APIs: Break down silos between origination, core banking, credit bureaus, and document management. Data flows seamlessly across platforms without manual exports, imports, or reconciliation.

For the broader context on lending workflow transformation, see our digital lending blogs.

Building a Faster, Smarter Loan Approval Process

Implementation doesn't mean ripping out existing systems. It means connecting them intelligently.

Start by mapping current bottlenecks. Where do applications sit longest? Which manual tasks consume the most hours? What information takes the longest to gather? Measure baseline timelines by loan type so you know what "better" looks like.

Prioritize high-volume, standardized products for initial automation. Equipment financing, working capital lines under $250K, and SBA loans benefit most from workflow optimization. Prove ROI on simpler products before tackling complex commercial real estate or syndicated deals.

Invest in platforms, not point solutions. Bolt-on tools that automate one step while leaving others manual create new integration headaches. Unified platforms that handle origination through servicing eliminate fragmentation and compound efficiency gains.

Train teams on new workflows. Technology enables speed, but people deliver it. Underwriters need to trust automated financial spreading. Relationship managers need to understand how digital portals enhance service, not replace relationships. Change management determines whether platforms deliver value or create resistance.

This is where platforms like Finspectra stand out: unified architecture that connects application intake, credit analysis, decisioning, and documentation in one system. Automated workflows that eliminate manual handoffs. Real-time visibility that keeps stakeholders informed without constant status meetings. Finspectra's Prizm Lending Suite delivers the operational efficiency that turns weeks into days without compromising credit quality.

Ready to see how it works? Book a demo and explore how Prizm enables faster approvals, better customer experiences, and scalable growth.

FAQs

- Can loan approvals be completed within minutes?

Yes, loan approvals can be completed within minutes for standardized products with automated decisioning. Small-dollar loans meeting pre-defined credit criteria can receive instant approvals through rule-based engines. Complex commercial loans requiring human judgment still need underwriter review, but digital platforms reduce timelines from weeks to days by eliminating manual data aggregation and workflow delays.

- How do lenders balance speed with risk in loan approvals?

Speed comes from eliminating operational friction, not loosening credit standards. Automated financial spreading, real-time credit bureau integration, and rule-based exception routing accelerate underwriting without compromising analysis quality. Underwriters spend less time gathering data and more time assessing risk.

- What data sources help speed up loan decisions?

To speed up loan decisions, integrated platforms that connect core banking systems, credit bureaus, accounting software (QuickBooks, Xero), and document management eliminate manual data collection. APIs enable real-time financial data access with borrower permission. Automated collateral valuation services and covenant monitoring tools provide instant risk context.

- Do faster loan approvals increase default risk?

No, faster loan approvals don’t increase default risk. Faster approvals result from better data access and automated workflows, not reduced diligence. Digital platforms improve credit quality by standardizing ratio calculations, flagging exceptions consistently, and maintaining complete audit trails. Speed and rigor aren't trade-offs when systems eliminate waste.

- How can lenders track loan approval efficiency?

To track loan approval process efficiency, lenders can measure key metrics like application-to-decision time by loan type, document collection cycle time, underwriting hours per application, credit committee throughput, and approval rate by underwriter. Modern platforms provide real-time dashboards showing where applications sit, which bottlenecks exist, and how timelines compare across products and teams.

.png)

.png)

.png)