%201.avif)

The New Reality: Lending in a Digital, Multi-Market World and where Loan Management Systems Fit in

A loan management system (LMS) is software that helps lenders manage the entire loan lifecycle, from origination and disbursement to servicing, monitoring, and closure. In this guide, we explain what a loan management system is, how it works across the loan lifecycle, the key features lenders should look for, and how the right LMS helps financial institutions operate more efficiently while staying compliant.

The New Reality: Lending in a Digital, Multi-Market World and Where Loan Management Systems Fit in

Picture this: a borrower applies for a loan on their phone at midnight, expecting approval in minutes and disbursal the next morning. Not long ago, this would have sounded unrealistic. Today, it’s standard. In Australia, 99.3% of customer-bank interactions are now digital. In the U.S., total consumer credit outstanding reached US$5.06 trillion as of mid-2025, highlighting the growing scale of borrowing activity that lenders must manage effectively

Borrowers expect speed, transparency, and flexibility, and regulators demand airtight compliance. The problem is that most traditional lending systems weren’t built for this dual pressure, leaving lenders caught between growing customer demands and escalating oversight.

Every delay risks a lost customer, and every oversight risks a regulatory fine. That’s where a loan management system (LMS) comes into the picture: a purpose-built loan system designed to streamline the entire loan management process across the lending lifecycle.

Every delay risks a lost customer, and every oversight risks a regulatory fine. That’s where the Loan Management System (LMS) comes into the picture: a purpose-built platform designed to help lenders operate intelligently across the entire loan lifecycle.

Defining Loan Management Systems: More Than Just Software

A loan management system is software that manages the full lifecycle of a loan, including origination, disbursement, servicing, repayment tracking, and closure within one platform. It helps lenders automate workflows, monitor loan performance, and ensure regulatory compliance while improving borrower experience.

A modern loan management system (LMS) isn’t just a loan servicing system that manages repayments after approval; it’s designed to handle the entire lending cycle.

A modern Loan Management System (LMS) isn’t just about servicing loans after approval; it’s designed to handle the entire lending cycle.

From application intake and origination to repayment scheduling, monitoring, collections, and closure, a robust lending management system brings the entire loan lifecycle under one roof.

From application intake and origination to repayment scheduling, monitoring, collections, and closure, a robust LMS brings everything under one roof.

In practice, that means the Loan Origination System (LOS) is no longer a separate, bolt-on platform. Instead, a good LMS comes with inbuilt loan origination capabilities, ensuring lenders manage the full borrower journey seamlessly. With lending intelligence woven into this process, lenders not only automate tasks but also gain sharper insights into risk, compliance, and borrower behavior.

This unified approach matters because gaps between loan origination and servicing are where many lenders face compliance issues or delinquency spikes. By embedding origination within the LMS itself, lenders gain visibility and control from day one, setting the stage for why loan management systems LMS matters now more than ever in key markets.

Loan Management System vs Loan Origination System

Although the terms are often used interchangeably, a Loan Origination System (LOS) and a Loan Management System (LMS) serve different roles within the lending lifecycle.

Many modern lending platforms combine LOS and LMS capabilities to provide a unified lending experience.

Why Loan Management Systems Matter Now More Than Ever

Modern lenders rely on loan management systems to automate the loan management process, reduce manual work, monitor risk in real time, and deliver faster digital lending experiences. Without a centralized system, lenders struggle with compliance, operational inefficiencies, and fragmented borrower data.

Building on this unified view of origination and servicing, the next question is: why does it matter so urgently right now? Lending today, is being reshaped by critical shifts that highlight the immediate need for a strong LMS:

- Regulation tightening: Regulators are increasing scrutiny on transparency, reporting, and consumer protection. For example, in New Zealand, the Credit Contracts and Consumer Finance Act (CCCFA) has tightened requirements on affordability and lender responsibility. Without an LMS that automates compliance and tracks every transaction, lenders risk penalties and reputational damage.

- Digital adoption: As noted earlier, with most borrower interactions moving online, lenders need digital lending systems that support self-service portals, digital wallets, and always-on access. A smart loan management system bridges this demand, ensuring consistent borrower experiences across channels.

- Economic headwinds: Rising consumer debt and loan write-offs (e.g., US$111.7 billion in U.S. non-mortgage debt write-offs in 2023) show how quickly risk can escalate. An LMS helps lenders monitor accounts in real time and intervene before defaults spiral.

Together, these shifts make it clear: waiting is no longer an option. The combination of stricter oversight, rising borrower expectations, and mounting credit risk is already reshaping competition in lending. Lenders that embrace a modern loan management system gain the ability to stay compliant under pressure, deliver seamless digital lending experiences, and protect margins even in volatile conditions. So what are the features an intelligent LMS should provide?

Key Features of a Loan Management System What Makes a Modern LMS: Core Features That Create Edge

The most effective loan management systems combine automation, monitoring, compliance controls, and borrower self-service tools to streamline the entire loan lifecycle. These features help lenders improve efficiency, reduce risk, and manage loan portfolios at scale.

The urgency we just explored brings us to the question of how lenders can actually meet these challenges. This is where the core features of a modern LMS step in. Rather than being a back-office tool, the LMS becomes the foundation that enables lenders to run faster, smarter, and with greater confidence. These loan management software features are designed to solve operational pain points that legacy lending systems simply cannot handle. Each feature is designed to solve a pain point that legacy systems simply cannot handle.

- Automation & Workflow Management: Automation goes beyond sending reminders. It eliminates repetitive tasks, ensures repayment schedules are accurate, and reduces reliance on manual processes and checks. This not only lowers labor costs but also frees up teams to focus on high-value decisions rather than chasing paperwork.

- Loan Tracking & Monitoring: A modern LMS acts as a powerful loan tracking system, providing real-time visibility into every account across the portfolio. Acting as a real-time loan monitoring system, early warning dashboards flag delinquencies before they spiral, allowing lenders to act quickly and reduce write-offs. A modern LMS provides real-time visibility into every account. Early warning dashboards flag delinquencies before they spiral, allowing lenders to act quickly and reduce write-offs. This proactive monitoring directly translates to healthier portfolios and lower risk exposure.

- Compliance & Risk Tools: Built-in KYC, AML, and region-specific reporting features ensure that lenders stay aligned with regulatory requirements. Instead of scrambling to prepare disclosures or audits, compliance becomes part of day-to-day operations, reducing both fines and reputational risk.

- Flexible Loan Servicing: Borrowers expect flexibility, whether it’s rescheduling payments, early closures, or managing deferments. An LMS that supports loan tracking and multiple repayment structures not only improves customer experience but also strengthens retention in competitive markets.

- Analytics & Reporting: Rich reporting capabilities allow lenders to forecast defaults, segment borrowers, and identify profitability drivers. With portfolio-wide insights, lenders can make data-backed decisions that directly protect margins and fuel growth.

- Ecosystem Integrations: APIs seamlessly connect the LMS with payment gateways, credit bureaus, and identity verification tools. These integrations streamline the loan lifecycle, reducing friction and ensuring data accuracy across all platforms.

- Cloud-Native Scalability: As loan volumes grow, a cloud-native LMS scales effortlessly. It supports remote teams, reduces infrastructure costs, and ensures lenders can expand into new markets without being held back by outdated systems.

Taken together, these features don’t just deliver efficiency, they provide lenders with the intelligence needed to adapt, compete, and grow. In other words, they form the backbone of a smarter, more connected way of lending, where operational control and strategic insight come together naturally.

Together, these features aren’t just checkboxes; they come to life when applied across the entire lending journey. That’s where an LMS shows its real impact: in how it transforms the loan lifecycle end to end.

Modern lending platforms are increasingly designed to combine these capabilities into a unified ecosystem. Solutions like Finspectra’s PRIZM Lending Suite integrate loan origination, loan management, analytics, and compliance tools into a single platform, helping lenders manage the full lifecycle without relying on fragmented systems.

How Loan Management Systems Transform the Loan Lifecycle

The features we just explored show their real value when applied across the full loan management process, from application capture to loan closure. The features we just explored only show their true power when applied across the full loan journey. Think of loan management like trying to navigate with a blurry map. An LMS clears the picture by adding a layer of lending intelligence through automation, adaptability, and risk insight, so when the moment comes to act, you do it with precision and certainty. And this is what lending intelligence really is.

Here’s how that plays out step by step:

- Application Capture: With integrated identity verification and credit bureau checks, onboarding becomes faster and more secure. Borrowers get quick responses, and lenders cut down on fraud or incomplete applications.

- Underwriting & Decisioning: Automation enhances speed while customizable scoring models reflect local borrower behavior. This balance reduces approval times and ensures that credit decisions are both quick and sound.

- Disbursement: Accurate and timely fund transfers remove one of the biggest borrower frustrations: delays. Lenders benefit from smoother cash flow management and reduced operational errors.

- Servicing & Collections: Automated reminders, personalized communication, and flexible repayment options help prevent delinquency. For lenders, this translates into higher recovery rates and stronger borrower relationships.

- Monitoring & Reporting: Real-time dashboards keep lenders aligned with regulatory obligations while providing insights into portfolio health. Early detection of risks means fewer surprises and better preparedness.

- Closure / Payoff: Transparent payoff statements and easy management of early settlements give borrowers clarity. Lenders, in turn, strengthen trust and free up resources for new originations.

When connected end to end, these stages showcase the true strength of lending intelligence where every decision is informed, every risk is visible, and every borrower interaction is smoother. This holistic impact sets the stage for why not having a powerful loan management system carries hidden costs that no lender can afford to ignore.

The Hidden Costs of Not Having a Powerful Loan Management System

Behind every delay or error in loan management lies a cost that lenders often underestimate until it affects profitability. Behind every delay or error in a loan process lies a cost, one that most lenders don’t account for until it hurts profitability or reputation. Sticking with outdated systems doesn’t just slow things down; it creates a cascade of risks that steadily weaken a lending business. Here’s where those hidden costs show up most clearly:

- Operational drag: Manual processes and disconnected tools slow down every stage, from repayment scheduling to collections. Over time, the added labor costs and frequent errors chip away at efficiency and reduce overall margins.

- Compliance exposure: When reporting depends on spreadsheets or manual updates, deadlines are often missed and data accuracy is compromised. This leads to regulatory fines, strained audits, and a weakened reputation with both regulators and investors.

- Poor borrower experience: Late disbursals, confusing statements, or repayment errors frustrate customers. Dissatisfied borrowers are less likely to stay loyal and more likely to choose competitors who offer smoother digital-first services.

- Financial risk: Without proactive monitoring, delinquent accounts can slip under the radar until defaults pile up. The result is higher write-offs and direct hits to profitability that could have been prevented with timely intervention.

The cumulative effect of these costs is far greater than the investment required for a modern LMS. By contrast, a platform that provides you with a holistic view of your lending operations turns these risks into opportunities for efficiency and resilience. Recognizing these hidden costs is the first step toward eliminating data silos and evaluating what truly matters when choosing a loan management system.

This is why many lenders are moving toward centralized lending platforms that eliminate data silos and automate servicing operations. Platforms built with modern loan management capabilities help institutions gain real-time portfolio visibility while reducing operational overhead.

What to Look for When Choosing a Loan Management System

Not every LMS will deliver the same results, and the wrong choice can leave lenders stuck with the very problems they set out to solve. Too often, lenders switch platforms only to find the same inefficiencies: manual workarounds, reporting blind spots, and limited borrower visibility, still slowing them down.

The right evaluation criteria ensure that an LMS is not only fit for today’s needs but also future-proof.

These are the essentials that separate the right LMS from less-capable alternatives:

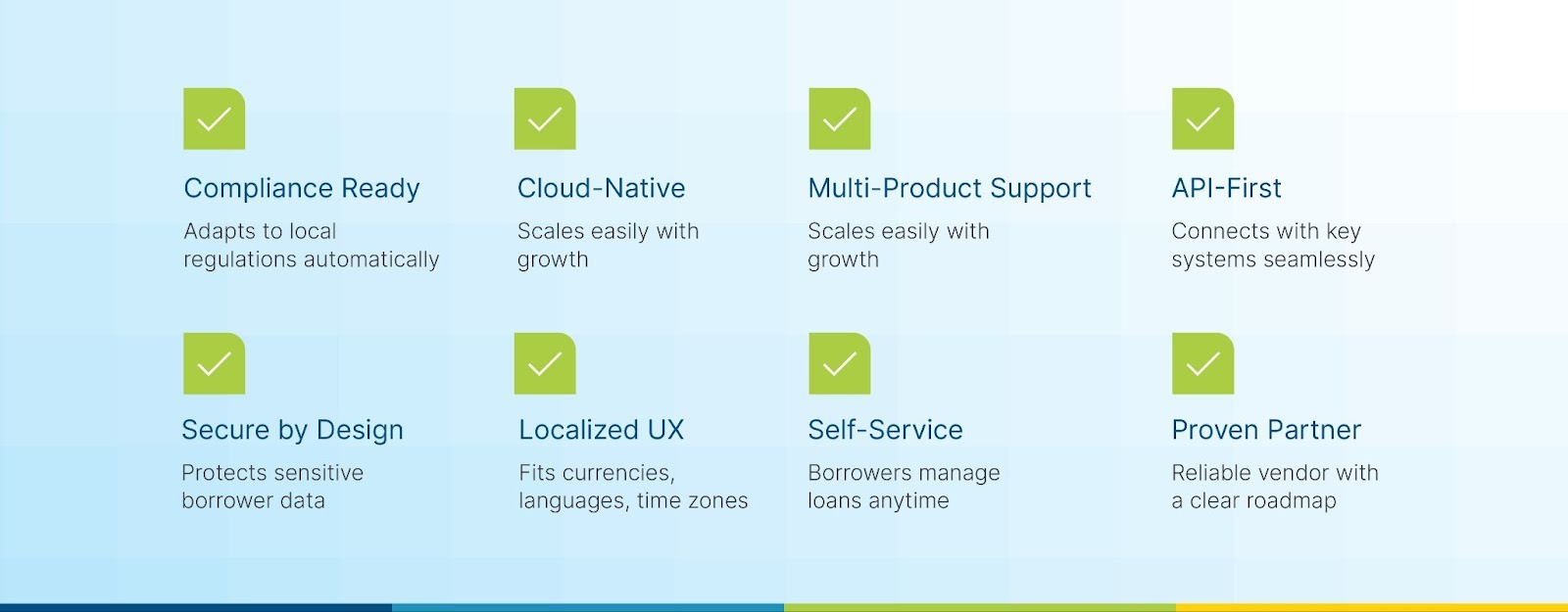

- Local compliance support: Each market has its own regulatory environment, and missing local nuances can lead to costly fines. A strong LMS automates compliance and adapts quickly to regulatory updates, keeping lenders always audit-ready.

- Cloud-native architecture: Growth should never be capped by infrastructure. Cloud-native systems scale seamlessly, reduce IT overhead, and enable secure remote access: critical for lenders expanding portfolios or operating across regions.

- Support for multiple loan products: From business loans to CRE loans or asset financing, lenders need flexibility. An LMS that supports varied structures allows businesses to diversify offerings without adding operational complexity.

- Strong API ecosystem: No system works in isolation. APIs allow the LMS to integrate with credit bureaus, payment gateways, and identity verification tools, ensuring smooth data flow and reducing manual input errors.

- Security features: Borrowers trust lenders with sensitive data. Features that align with regional privacy laws and advanced security measures protect that trust and reduce the risk of breaches.

- Localized user experience: Currencies, languages, and time zones matter. A localized LMS ensures borrowers and internal teams have frictionless experiences that fit their context.

- Self-service portals: Modern borrowers expect control at their fingertips. Self-service features like viewing balances, making payments, or checking payoff statements reduce support calls and boost satisfaction.

- Vendor roadmap and reliability: Choosing a partner is as important as choosing a platform. A clear product roadmap and proven track record give lenders confidence that the LMS will keep evolving with their needs.

Bring these elements together and you get more than a tool; you get the structure to make smarter choices, serve customers better, and grow without losing control.. It’s here that lending intelligence quietly comes to life, preparing the ground for understanding the trends that will define and forecast the future of lending.

What’s Coming Next: Trends Shaping Loan Management Systems

Lending continues to evolve. Even with the right LMS in place, technology and borrower expectations continue to evolve. For lenders, this means keeping an eye on emerging developments that are set to redefine the industry.

While not all providers cover these areas yet, understanding them helps decision-makers prepare for the future of lending and scalable growth opportunities:

- AI-driven risk scoring: Artificial intelligence is moving beyond simple credit checks to deliver predictive insights into borrower behavior. By spotting patterns earlier, lenders can act before delinquency escalates, reducing defaults and improving portfolio health.

- Embedded finance and POS lending: Borrowers increasingly want credit embedded directly at the point of sale, whether online or in-store. Lenders that can plug into these ecosystems create new revenue streams and capture borrowers in the moment of need.

- Regtech innovations: Compliance continues to be one of the heaviest burdens on lenders. Regtech tools promise automation of reporting, monitoring, and regulatory filings at scale, cutting down compliance costs while minimizing human error.

- Customer-first design: Beyond servicing loans, borrowers now expect intuitive mobile apps, self-service dashboards, and transparency across every touchpoint. This shift emphasizes user experience as much as operational capability.

These trends point to a future where lending evolves even further, expanding beyond efficiency into predictive, compliance-first, and highly personalized lending workflows. Recognizing what’s coming next makes it clear why staying static isn’t an option and leads directly into why lenders must act without delay.

Conclusion: Why Lenders Shouldn’t Wait

From rising borrower expectations to tightening regulatory oversight and the very real cost of defaults, the message is clear: the old way of managing loans no longer supports lenders’ growth. Every section we’ve explored points to the same truth: lenders need a system that provides control, visibility, and adaptability across the entire lifecycle.

On a global scale, the risks of delay are steep, but the opportunity is even greater. A modern loan management system offers more than operational efficiency; it builds trust, ensures compliance, and strengthens resilience in uncertain markets. Put simply, it’s the difference between fixing issues early and letting them grow into costly setbacks. This is the essence of lending intelligence in action.

Ready to see how it works in practice? [Book a Demo] and explore how Finspectra’s PRIZM Lending Suite helps lenders gain control, speed, and clarity across their loan portfolios.

FAQs

1) What is the loan management system?

Loan management refers to the process of handling the full lifecycle of a loan, from origination and disbursement to servicing, monitoring, and closure. A loan management system (LMS) is the software that automates and manages this process. A loan management system (LMS) is software that manages the entire loan cycle, from origination to servicing and closure, in one platform.

2) How does LMS enhance compliance with financial regulations?

An LMS automates reporting, tracks every transaction, and includes built-in KYC/AML checks to keep lenders aligned with regulations.

3) What benefits do cloud-based loan management systems provide?

Cloud-based LMS platforms scale easily, reduce IT costs, and allow secure access for teams and borrowers anytime, anywhere.

4) How can lenders optimize loan disbursement processes?

By using an LMS, lenders can automate fund transfers, reduce errors, and ensure borrowers receive disbursals quickly and accurately.

.png)

.png)

.png)