%201.avif)

Unified Lending Platforms vs Patchwork Systems: The Real Cost of Scaling SME Lending

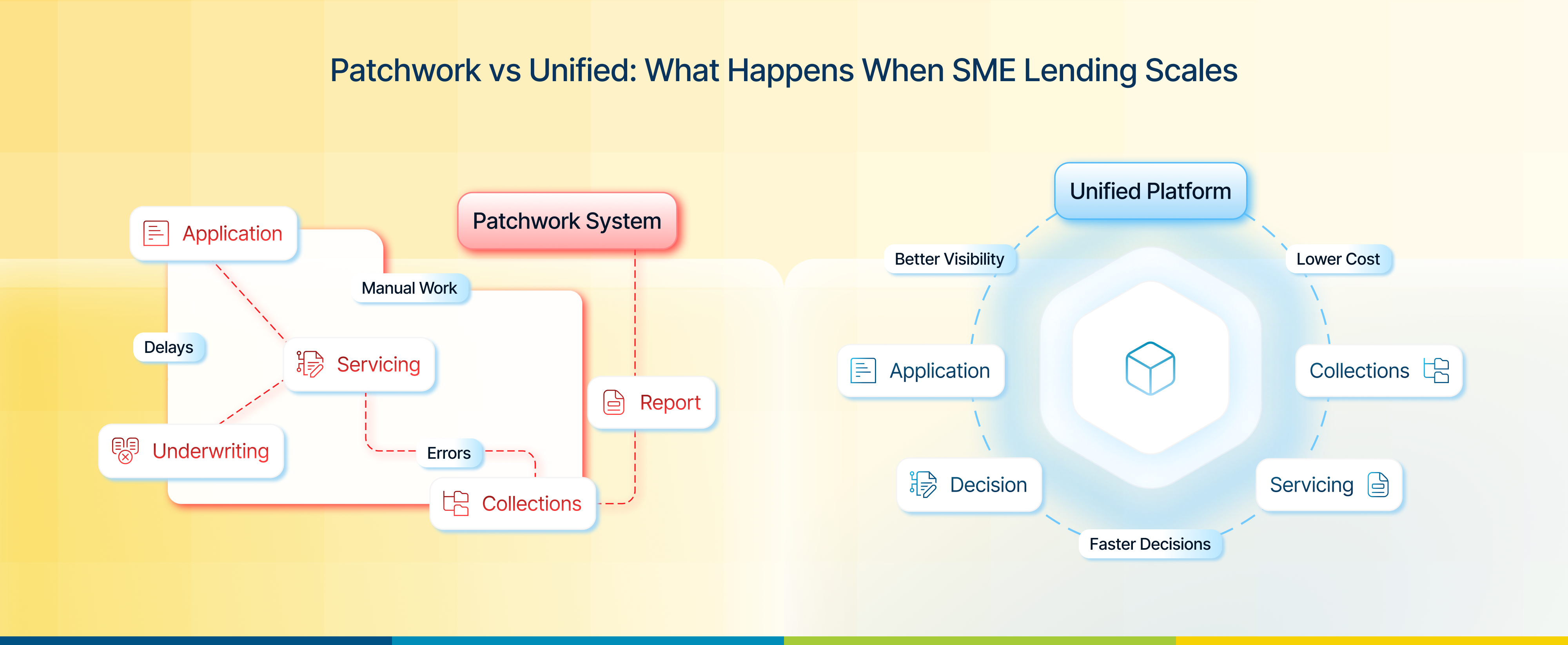

What Are Patchwork Lending Systems?

Patchwork lending systems are built by combining multiple platforms and manual processes to manage the loan lifecycle.

A typical setup may include:

- A standalone loan origination system

- Spreadsheets for underwriting or tracking exceptions

- Separate servicing software

- External tools for collections

- Custom integrations and manual data transfers

This structure works at low volumes. But as portfolios grow, the lack of coordination between systems begins to slow operations and increase risk.

Many lenders don’t start fragmented. In fact, fragmentation happens gradually as new products, partners, and regulatory requirements are added over time.

Why Patchwork Lending Systems Fail at Scale

Fragmented environments create operational drag at every stage of the lifecycle.

1. Rising Operational Costs

When systems don’t communicate, teams spend time reconciling data, moving information manually, and resolving errors.

Common cost drivers include:

- Duplicate data entry across systems

- Manual report preparation

- Exception handling and rework

- Larger operations teams to manage handoffs

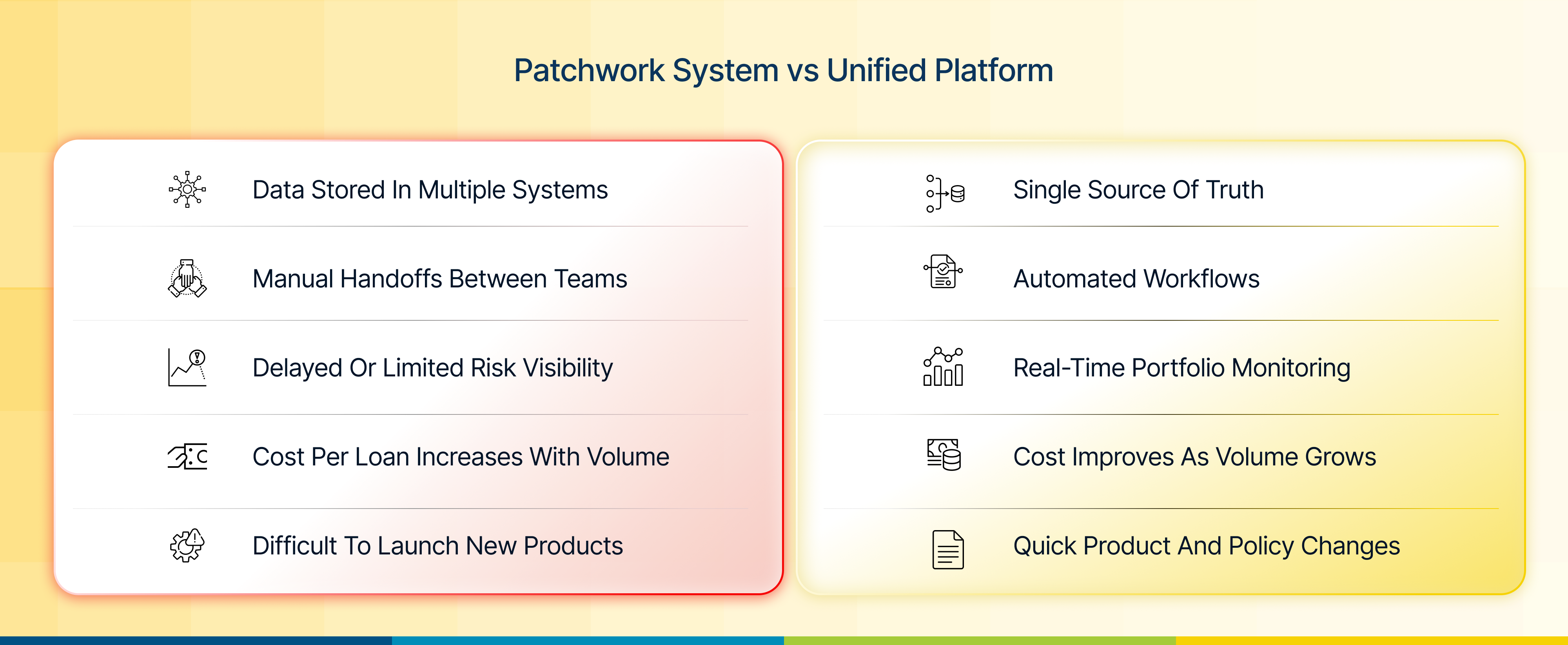

As volumes increase, the cost per loan rises instead of improving with scale.

2. Data Silos and Limited Risk Visibility

In patchwork environments, borrower and portfolio data sit in different systems. Leadership often relies on delayed or manually consolidated reports.

This creates:

- Incomplete borrower views

- Slow identification of early stress signals

- Inconsistent risk assessment across products

- Limited portfolio-level monitoring

Fragmentation increases the hidden costs of data silos, including higher NPAs and delayed corrective action.

3. Slower Decisioning and Poor Customer Experience

SMEs expect faster approvals and clear communication. But fragmented workflows create multiple handoffs between teams and systems.

The result:

- Longer turnaround times

- Frequent document re-requests

- Limited status visibility for borrowers

- Higher drop-offs during processing

Scaling volume without integrated workflows often leads to declining customer experience.

4. Compliance and Audit Pressure

Regulatory expectations increase as SME portfolios grow. In fragmented environments, audit trails are scattered across systems and manual records.

Teams spend significant time:

- Tracing decisions across platforms

- Reconciling data discrepancies

- Preparing regulatory reports

- Managing policy changes manually

Compliance becomes reactive instead of controlled.

The Hidden Cost of Integration Overhead

Many lenders try to solve fragmentation through integrations. But maintaining multiple point-to-point connections adds its own complexity.

Over time, lending system integrations can create:

- High maintenance effort

- Dependency on IT for routine changes

- Upgrade challenges across vendors

- Increased risk of data failures

Instead of simplifying operations, the ecosystem becomes harder to manage.

What Is a Unified Lending Platform?

A unified lending platform brings the entire SME loan lifecycle onto a single system — from application and underwriting to servicing, monitoring, and collections.

An end-to-end lending platform provides:

- A single borrower and loan record

- Automated workflows across stages

- Real-time portfolio visibility

- Centralized policy and product configuration

- Built-in audit trails and compliance controls

Rather than connecting multiple tools, lenders operate within one coordinated environment.

How Unified Platforms Change the Economics of SME Lending

The value of a unified architecture isn’t just operational convenience. It changes how lending businesses scale.

Lower cost per loan

Automation reduces manual work, rework, and reconciliation effort.

Faster decision cycles

Integrated data and rules enable quicker underwriting and approvals.

Better risk control

Real-time monitoring allows early intervention and consistent portfolio oversight.

Operational scalability

New products, volume increases, and regulatory changes can be managed without expanding headcount proportionally.

For growing portfolios, this shift from fragmented tools to scalable lending software directly improves unit economics.

Unified vs Patchwork: The Scaling Difference

This difference becomes critical when portfolios grow rapidly or when lenders expand into new SME segments.

Is Migration to a Unified Platform Risky?

Migration is often seen as disruptive, but the larger risk is staying fragmented while volumes increase.

A phased approach, starting with high-impact lifecycle stages such as origination or servicing, allows lenders to transition without operational disruption.

Modern business lending software is designed to support:

- Parallel system operation during transition

- Data migration and validation

- Configurable workflows to match existing processes

- Integration with core systems where required

For many lenders, the operational risk of fragmentation eventually outweighs the transition effort.

When to Consider Moving Away from Patchwork Systems

Technology consolidation becomes urgent when lenders experience:

- Rising cost per loan despite automation efforts

- Increasing turnaround times

- Limited portfolio visibility

- High manual reporting effort

- Difficulty launching new SME products

These signals often indicate that the current stack is constraining growth.

The Bottom Line

Patchwork lending systems are often the result of growth. But beyond a certain scale, fragmentation begins to increase operational cost, risk exposure, and decision delays.

A unified SME lending platform doesn’t just replace multiple tools. It creates a coordinated operating model where automation, visibility, and control improve as volumes grow.

For fintech lenders scaling SME portfolios, the real question isn’t whether systems work today; it’s whether the current architecture can support growth without increasing complexity tomorrow.

.png)

.png)

.png)