%201.avif)

Asset Financing 101: How Lending Software Simplifies the Process

In today’s capital-constrained environment, many small and medium enterprises (SMEs) and non-bank lenders are struggling to scale using unsecured credit alone. Macroeconomic volatility, tightening interest rates, and higher credit risk have forced players to rethink their lending models.

Asset financing (also known as asset-based lending) presents an opportunity: it gives lenders a built-in recovery buffer by tying credit to physical or financial collateral. But executing it at scale is operationally complex. That’s why modern lending software is the engine that makes scalable, risk-controlled asset lending possible.

To frame the scale of the opportunity: in emerging and developing markets, the SME finance gap is estimated at USD 5.7 trillion across formal MSMEs. That’s a huge underserved market, and asset-backed models are one of the tools to bridge it.

In this guide, we’ll cover:

- What asset financing / asset-based lending is

- Why it matters to fintechs / SME lenders

- The manual (legacy) process vs. software-enabled process

- Key software capabilities and their business impact

- Implementation risks, future trends, and how Finspectra fits into the picture

What Is Asset Financing / Asset-Based Lending?

Definition & Core Principle

Asset financing refers to forms of lending or leasing where the borrower uses one or more assets as collateral (or as the financed asset). The collateral helps reduce lender risk, because if the borrower defaults, the lender may seize or liquidate the asset.

Unlike unsecured lending, where credit decisions rely primarily on cash flows, credit history, and business metrics, asset-based lending gives the lender an additional “floor” via the underlying asset value.

Forms of Asset Financing

Asset financing isn’t one-size-fits-all. Some common forms:

- Secured Loans / Asset-Backed Lending: Borrower owns or acquires the asset; it’s pledged as security.

- Hire Purchase / Installment Finance: Borrower pays in installments, often after putting down a deposit; ownership transfers after payments.

- Lease / Finance Lease / Operating Lease: Lender retains ownership; borrower uses the asset for a period. At lease-end, there may be a purchase option.

- Sale-and-Leaseback: Borrower sells an owned asset to the lender and leases it back, freeing up capital while retaining usage.

- Refinancing / Releveraging: Borrowers may borrow against assets they already own to restructure liabilities or extract liquidity.

Each variant has trade-offs in terms of risk, accounting treatment, control, residual value, and enforcement complexity.

Asset Types & Valuation Complexity

Assets can vary widely: machinery, vehicles, plant & equipment, inventory, accounts receivable, even specialized industrial assets. The more exotic or illiquid an asset, the more conservative the lender’s valuation and liquidation assumption must be.

An asset’s depreciation path, maintenance records, utilization history, residual demand, regional resale market — all matter. That complexity is exactly what makes asset financing powerful but also operationally demanding.

Why Lenders & Fintechs Care

- Better risk buffer vs unsecured lending

- Works well when borrowers have limited free cash flows but own meaningful assets

- Enables product innovation (e.g. usage-based leases, hybrid models)

- Allows scaling in regions or sectors underserved by unsecured models

But to do this well, lenders must handle process complexity, data integrations, collateral monitoring, defaults, and accounting — which is where software comes in.

The Legacy (Manual) Asset Financing Process: Where Things Break

To appreciate what software brings, let’s map how asset finance is typically done in a non-digital, manual setup:

- Application & Preliminary Assessment

Capture borrower data, business plan, asset request, financials. - Collateral Appraisal / Inspection

Engage third-party appraisers, inspect the asset physically, collect papers (title, maintenance records). - Underwriting / Credit Decision

Combine financial analysis, credit history, and collateral value to decide limits. - Legal Documentation, Security Filings

Prepare security agreements, UCC / local lien filings, title registration. - Disbursement / Asset Delivery

Fund the purchase or lease the asset; ensure legal title transfer or lease contract. - Servicing / Monitoring

Track payments, monitor collateral health, aging, depreciation, usage. Trigger alerts if metrics drift. - Default / Recovery / Repossession

If payments fail, initiate repossession, legal processes, remarket or liquidate the asset. - Accounting, Reporting, Compliance

Reconcile payments, amortize depreciation, audit reporting, local regulatory compliance.

In this path, every handoff is a point of delay or error. Spreadsheets, manual approvals, document versioning, legal complexity and cross-team friction multiply. For a lender doing 50+ deals per month, operations become a bottleneck.

Common failure modes in manual setups:

- Inconsistent collateral valuation

- Repossession delays or legal leeway cost

- Poor audit trail or mis-accounting

- Scale limit due to manual overhead

- Poor cross-team visibility

So, to scale asset lending, manual methods fall short. The only way forward is automation, integration, workflows, and real-time monitoring.

How Modern Lending Software Simplifies Asset Financing

Modern software transforms each stage above. Below are the key domains where software adds leverage — with business impact.

1. Workflow & Orchestration Engine

A rules-driven engine automatically routes tasks: valuation requests, credit review, legal checks, approvals. Exceptions trigger human intervention; routine paths flow end-to-end. This eliminates handoffs and reduces TAT (turnaround time).

2. Collateral / Asset Lifecycle Module

Maintain an asset registry: metadata (make, model, serial, purchase date), depreciation curves, maintenance logs, residual valuations, usage metrics. Tie each asset to its loan contract.

You can track the health of the asset, usage, upkeep, and even interface with IoT/data feeds (if assets are smart machines) to monitor for wear or risk.

3. Automated Underwriting / Decisioning

Software ingests financial statements, credit bureau data, asset indices, historical loss data. A rule engine or ML model can score credit and collateral combination. You get consistent, scalable, repeatable decisions.

4. Real-Time Monitoring & Alerts

Once live, the software continuously monitors key metrics:

- LTV drift (if collateral value declines)

- Asset depreciation or impairment

- Payment delinquency patterns

- Maintenance compliance

- External risk signals (market declines, regulatory changes)

When thresholds are crossed, the system can flag or even run remedial workflows (e.g., request additional collateral, trigger top-up, issue warnings).

5. Recovery / Default & Repossession Workflows

Instead of ad-hoc recovery, the system can manage the entire default lifecycle: sending notifications, legal approvals, repossession orders, tracking auction / resale results, settlement accounting.

Everything is tracked at the case and asset level, with audit logs.

6. Accounting, GL Integration & Audit Trails

Automatic journal entries (interest accrual, principal amortization, depreciation, write-offs) flow into the general ledger or ERP system. The system provides audit logs, versioning, and regulatory reports, improving compliance and reducing manual reconciliation.

7. APIs & Integrations

A modern system isn’t siloed — it connects to:

- Credit bureaus / identity systems

- Appraisal services / asset price databases

- ERP / procurement systems

- IoT / sensor data (for smart assets)

- Legal / registries for lien / title filings

- Analytics / BI tools

This avoids manual rekeying, data mismatch, and enables richer automation.

8. Configurability & Geo-Scale Support

Rather than rigid modules, lenders need platforms they can configure: define asset classes, depreciation curves, decision rules, local legal workflows, compliance in multiple jurisdictions, multi-currency, and localization. A well-architected system scales across markets.

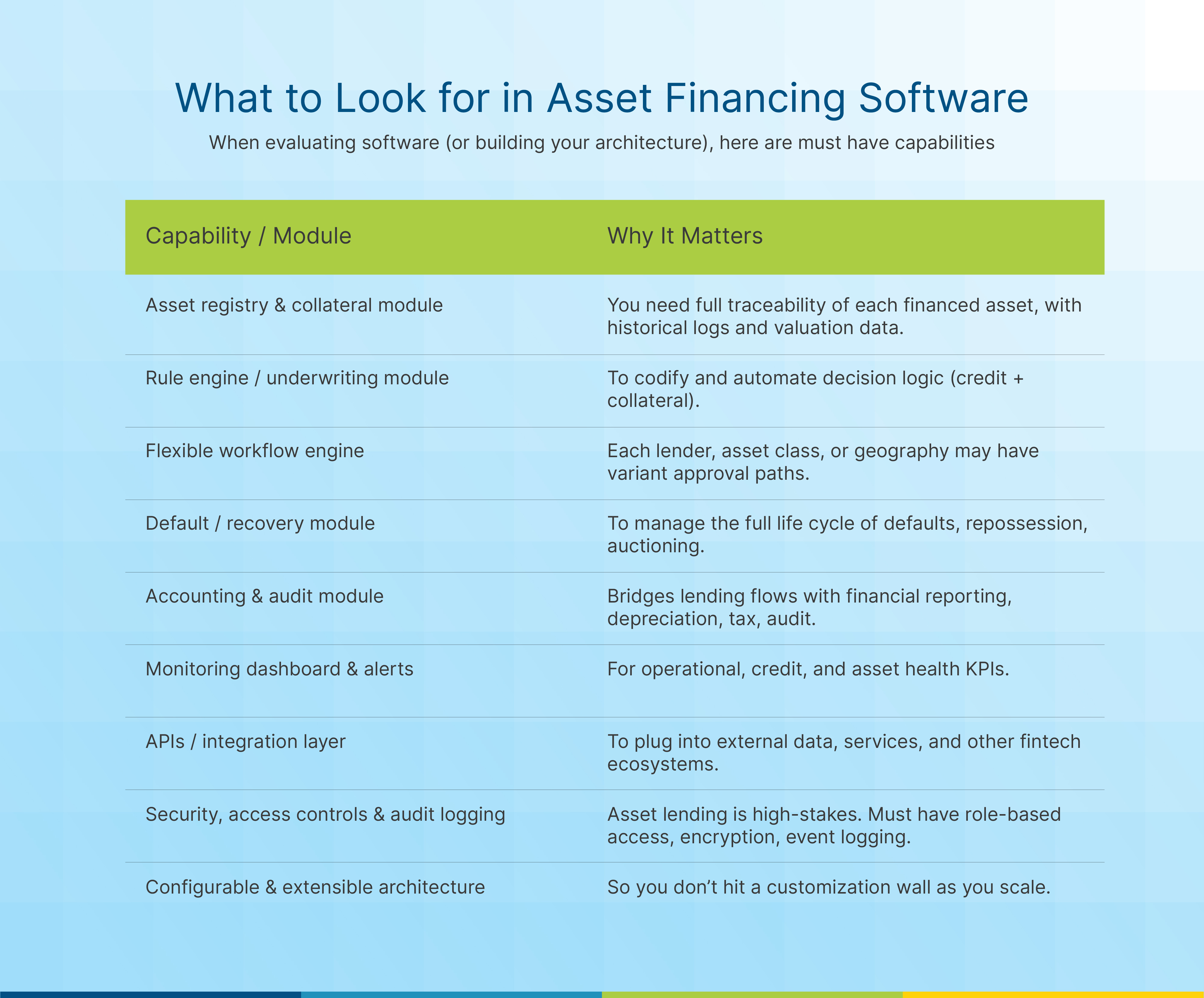

What to Look for in Asset Financing Software

When evaluating software (or building your architecture), here are must-have capabilities:

Business Impact & ROI of Software-Enabled Asset Finance

Let’s move from theory to metrics. What benefits does a software-first asset finance engine deliver?

- Dramatically reduced turnaround time

Manual processes may take days or weeks; software can compress that to hours or same-day for simpler deals. - Operational cost savings

Fewer manual tasks, fewer errors, lower headcount growth. Automation can cut costs by 30–40 % in certain lending workflows (for digital lending broadly). - Better risk control & lower NPLs

Dynamic collateral monitoring, early alerts, and automated interventions help prevent losses. - Scalability

You can scale volumes without a linear increase in operations staff — growth becomes higher-leverage. - Product flexibility & innovation

You can launch new lease variants, hybrid models, fractional financing, or usage-based models with agility. - Regulatory / audit readiness

Built-in traceability, audit logs, and compliance workflows reduce legal and regulatory risk. - Revenue upside / margin improvement

Because you reduce loss and cost, the net margin per deal improves; you can price more competitively.

Implementation & Deployment Considerations

Even the best software can fail if you don’t plan the implementation carefully. Here are risks and mitigations:

1. Data quality / legacy systems

- Your existing asset, borrower, accounting data may be fragmented, inconsistent or siloed.

- Mitigation: A data migration & normalization strategy, incremental rollout, cleansing steps.

2. Change management & stakeholder alignment

- Credit, legal, operations teams may resist new processes.

- Mitigation: Involve stakeholders early, provide training, pilot with limited asset classes, co-design workflows.

3. Customization vs. configurability trade-off

- Over-customizing can lead to maintenance burden and upgrade blocks.

- Mitigation: Favor platforms with strong built-in configurability and avoid heavy one-off hacks.

4. Legal, jurisdictional, and lien enforcement challenges

- In many markets, securitization, repossession rules, lien registration, and ownership transfer differ.

- Mitigation: External legal advisory, flexible workflow branching per geography, modular legal logic.

5. Security, privacy & regulatory risk

- Asset, borrower, collateral data is sensitive.

- Mitigation: Standardize on encryption, secure hosting, access control, auditing, and compliance (e.g. GDPR, local privacy laws).

6. Cost & ROI timeline

- Implementation often has upfront cost (customization, integrations).

- Mitigation: Phased rollout (start with high-volume, simpler asset classes), monitor ROI, plan for 2–3 year breakeven.

7. Integration complexity

- Tying into existing systems (ERP, procurement, credit bureaus) may be messy.

- Mitigation: Well-defined API boundaries, middleware, staging environments.

Hypothetical Use-Case: A Global SME Lender Scaling Asset Lending

To make this more concrete (without naming any real competitors), imagine:

- A mid-sized SME lender in Southeast Asia wants to launch equipment leasing (tractors, pumps, small machinery) across 3 countries.

- They deploy Finspectra’s platform as the lending engine.

- They upload asset classes with depreciation models.

- Configure underwriting rules (e.g. max 70% advance, age ≤ 7 years, maintenance history required).

- Integrate with local appraisers and registration authorities.

- Define country-specific workflows (e.g. legal checks, title registration, repossession paths).

- They upload asset classes with depreciation models.

- The system automates the path from application → appraisal → decision → disbursement → servicing → recovery.

- Real-time dashboards track utilization, LTV drift, performance per asset class.

- Within 6 months, the lender processes 3× deal volume with only 1.5× operations headcount. NPLs remain controlled due to proactive alerts and collateral monitoring.

This scenario is fully plausible if your software is built for configurability, scale, and global domains.

Future Trends in Asset Financing & Tech

Looking ahead, here are emerging trends reshaping the space:

- AI-powered valuation & predictive modeling

Algorithms that predict future residual value, failure / maintenance trends, market demand for used assets. - Tokenization & fractional collateralization

Collateral assets represented on-chain or via digital tokens, enabling fractional lending, collateral pooling, or shared risk pools. - Embedded asset financing

Equipment marketplaces, OEMs, or distributors offering financing at point-of-sale, via API integration (you buy the machine + lease it via platform). - IoT / sensor integration

Real-time telemetry from machines to monitor usage, condition, predictive maintenance — feeding into risk models. - Green asset finance & sustainability-linked leases

Lenders may offer favorable rates for assets aligned with ESG goals (e.g. solar equipment, electric vehicles). - Cross-border / multi-jurisdiction platforms

Lenders operating across geographies demand platforms that handle local compliances, languages, currencies, legal regimes.

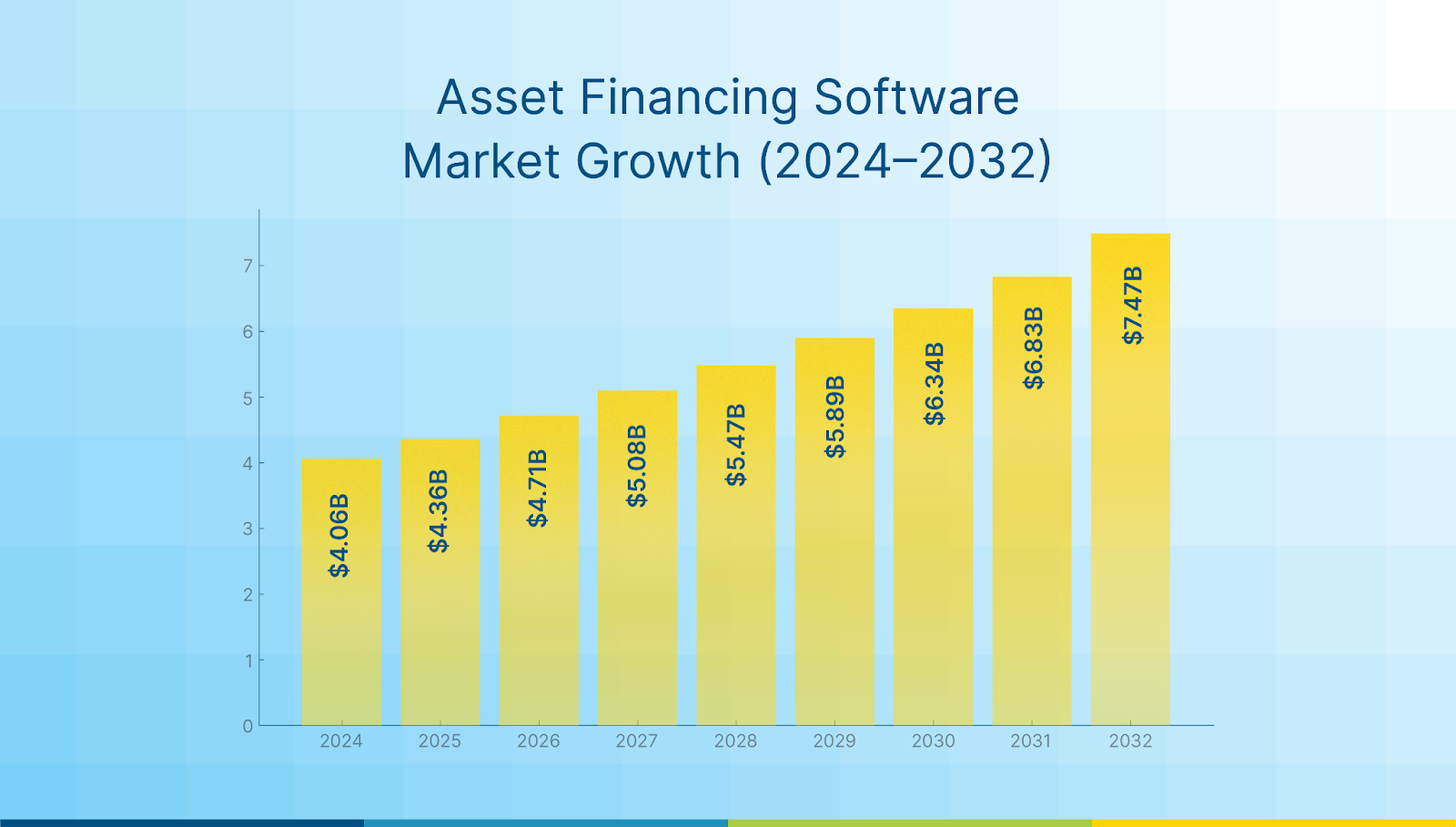

Given market momentum, the asset finance software market is growing rapidly as more lenders adopt digital models.

Conclusion

Asset financing is not new, but the scale, speed, and risk control that modern lending software enables is what’s new. For fintechs and SME lenders seeking to move beyond unsecured credit, software-driven asset lending offers the path to scale, automation, and profitability.

Manual processes leak efficiency, accuracy, and scalability. A well-architected lending platform becomes your competitive moat — enabling faster decisions, proactive risk management, and smoother operations.

.png)

.png)

.png)