%201.avif)

Loan Origination Software Explained: Features & Benefits

Getting a loan used to mean endless paperwork, branch visits, and waiting for approvals that crawled through multiple desks. Even after “digitization,” many lenders were still buried under disconnected tools — one for KYC, another for credit checks, and a third for disbursement. Efficiency improved, but the chaos never really went away.

Loan Origination Software changes this story. It acts as the command center for modern lending — managing every step from the borrower’s first click to the final disbursal. Instead of juggling spreadsheets or manual verifications, LOS automates the process, ensuring speed, compliance, and accuracy at scale.

At its simplest, LOS is a digital workflow engine built to handle the full loan journey: application intake, KYC verification, credit scoring, underwriting, decisioning, and audit tracking. But in practice, it’s much more than that — part data orchestrator, part compliance enforcer, and part decision assistant.

A modern LOS typically has three layers working together:

- Front-end: where customers or agents apply — web, app, or partner portals.

- Middleware: where business rules and credit decisions run.

- Back-end: where it connects to the institution’s core system for disbursal and reporting.

To clear up the usual confusion:

- LOS manages the loan approval process (before disbursal).

- LMS handles servicing and repayments (after disbursal).

- Core Lending Systems keep the financial backbone running in the background.

Together, they form the digital nervous system of a lender.

Result = faster approvals, cleaner audits, and happier customers — without adding more hands or hours. LOS isn’t about replacing people; it’s about freeing them to make better lending decisions.

Lending isn’t what it used to be. Borrowers now expect instant approvals, and lenders have to deliver speed without losing control or breaking compliance rules. It’s a delicate balance that manual processes can’t handle anymore.

The biggest pain points today? Rising defaults, disjointed systems, and ever-stricter regulations. Many lenders are still running on patchwork setups — one tool for KYC, another for underwriting, and a third for disbursal. It’s slow, error-prone, and impossible to scale.

A modern Loan Origination System brings order to that chaos. It centralizes every step of lending into a single, automated workflow that’s consistent, traceable, and audit-ready. With APIs, scoring engines, and rule-based decisioning, LOS helps lenders process loans faster, detect risk earlier, and stay compliant without constant firefighting.

In short, LOS isn’t a “nice upgrade” — it’s the foundation of sustainable lending in 2025. The right system lets lenders move with fintech-level speed while maintaining bank-level discipline.

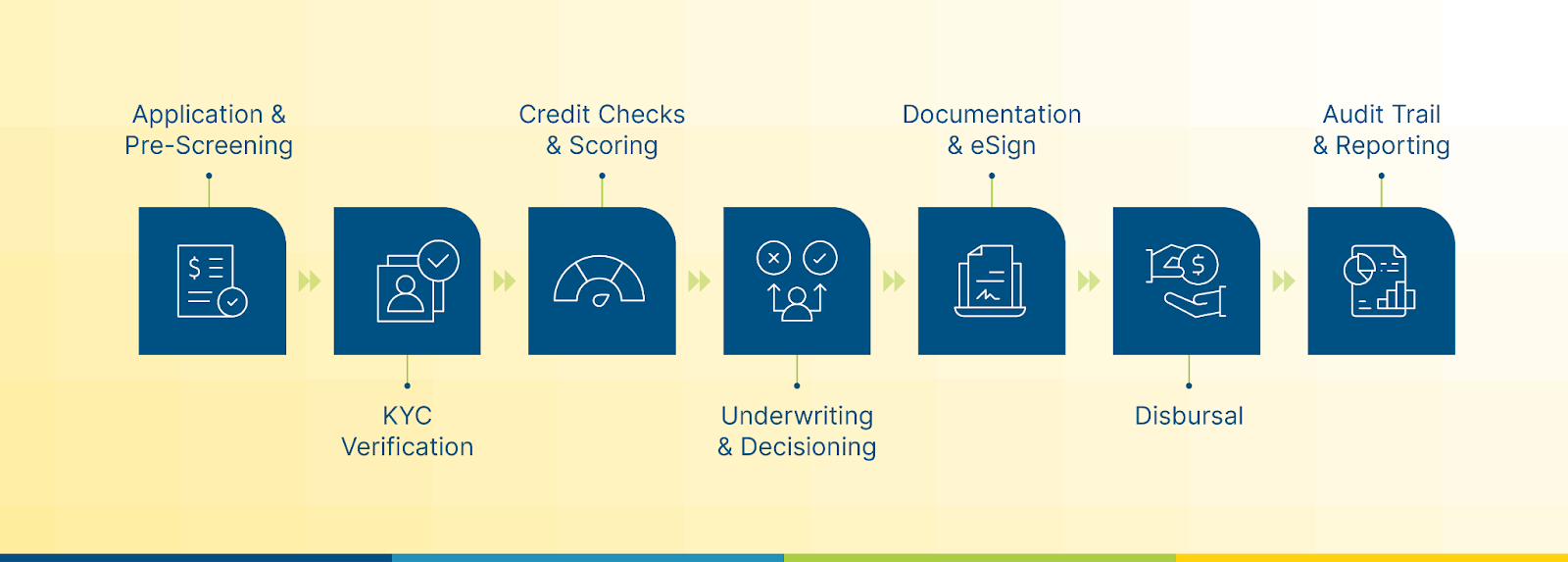

Loan Origination Workflow

Every loan goes through the same journey — the only difference is how efficiently it’s handled. A good LOS turns that journey into a smooth, predictable flow.

Here’s what that looks like:

- Application & Pre-Screening – The borrower fills out a digital form. The system checks basic eligibility and routes it to the right workflow.

- KYC Verification – Connects with Aadhaar, PAN, or CKYC to confirm identity in seconds.

- Credit Checks & Scoring – Pulls credit data from bureaus like CIBIL or CRIF and generates a risk score.

- Underwriting & Decisioning – Applies predefined rules or AI models to evaluate risk and automatically approve, reject, or escalate cases.

- Documentation & eSign – Generates digital loan agreements and triggers eSign or eMandate for auto-debits.

- Disbursal & Handoff – Sends approved data to the core lending system or LMS for release of funds.

- Audit Trail & Reporting – Logs every step, creating a complete digital footprint for compliance and analytics.

The framework stays the same across loan types — whether it’s retail, MSME, or mortgage. What changes are the rules, documents, and scoring models.

The best LOS platforms make this process invisible to the borrower — fast, accurate, and nearly frictionless.

Core Architecture of LO

A loan origination system isn’t a single app — it’s a stack of interconnected layers that handle data, decisions, and delivery.

At the top is the front-end, where customers or agents submit applications. The middleware layer processes those inputs, applying credit rules, decision engines, and workflow automation. The back-end connects with lending systems, credit bureaus, and reporting tools to keep everything synced.

APIs keep data flowing smoothly between these layers, while a rule engine ensures every decision follows policy. Add analytics dashboards and audit trails, and you get a system that’s transparent, scalable, and regulator-friendly.

In essence, LOS acts like the operating system of lending — integrating people, data, and compliance into one rhythm.

Key Features of Loan Origination Software

Every LOS claims to be “automated,” but the best ones deliver automation that lenders can trust. Here are the features that truly matter:

- Unified Application Management: One dashboard to view and manage all incoming applications from branches, partners, or digital channels.

- Automated Credit Scoring: Real-time integration with multiple credit bureaus and internal scoring logic for consistent risk evaluation.

- Workflow Automation: Configurable approval paths that remove manual routing and human bottlenecks.

- Document & Compliance Management: OCR, eKYC, and AML checks built directly into the workflow to keep audits clean.

- Analytics & Reporting: Dashboards that track TAT, rejection reasons, and risk distribution.

Other value-adds include fraud detection engines, flexible integrations with CRMs or core lending, and scalable cloud deployment.

The key is not having more features — it’s having the right ones working seamlessly together. A good LOS adapts to your lending model instead of forcing you to adapt to its limitations.

AI & Future-Ready Lending

AI is quietly reshaping how lenders make credit decisions. It doesn’t replace underwriters — it makes them sharper.

Machine learning models now analyze thousands of past loans to predict default risk. OCR and NLP tools read and validate income proofs or bank statements instantly. Robotic Process Automation (RPA) handles repetitive tasks like pulling bureau reports or generating sanction letters.

The more the system learns, the better it gets. Over time, AI-driven LOS platforms spot patterns humans can’t — early signs of fraud, shifts in borrower behavior, or gaps in credit policy.

It’s the difference between reacting to risk and anticipating it. In the near future, lenders won’t ask if their LOS uses AI — they’ll ask how well it learns.

Compliance and Risk Management

Lending runs on trust — and trust relies on compliance. Every lender, whether a company or a fintech, operates under layers of regulation designed to protect customers and ensure transparency.

A modern LOS builds compliance into its DNA. It automatically runs KYC, AML, and credit checks using verified APIs — Aadhaar, PAN, CKYC, or bureau integrations — and logs each step in an audit trail. That makes every approval traceable and every rejection explainable.

In India, compliance often revolves around RBI’s digital lending guidelines, CKYC, and data protection mandates. Globally, lenders also follow standards like GDPR, GLBA, or TILA, depending on where they operate. A strong LOS handles these frameworks without slowing operations down.

Instead of scrambling during audits, lenders can pull real-time compliance reports or filter transactions by risk category in seconds. LOS turns regulation from a roadblock into a safeguard — one that scales with your business.

Deployment, Integrations, and KPIs

Once a lender chooses LOS, two questions come next: Where will it run? and How will it connect?

Deployment Models

Most lenders today go for cloud-based systems — easy to deploy, secure, and scalable. Larger banks or public-sector entities might choose a hybrid model, keeping sensitive data on-premise while running workflows in the cloud. Either way, the goal is the same: quick setup, low maintenance, and zero downtime.

Integrations That Matter

LOS works best when it talks to other systems:

- Credit bureaus (CIBIL, CRIF, Experian) for real-time credit pulls.

- KYC APIs for instant identity verification.

- Banking and payments through eNACH, UPI, and account aggregators.

- CRM and LMS platforms like HubSpot or Salesforce, etc., for a seamless handoff post-disbursal.

Every integration trims a little more friction from the loan cycle — meaning fewer manual checks and faster disbursals.

Measuring Success

You can’t improve what you don’t measure. The top KPIs for LOS success are:

- Loan turnaround time (TAT) – How long it takes to go from application to disbursal.

- Approval-to-default ratio – The quality of your credit decisions.

- Compliance accuracy – How cleanly the system passes audits.

- Customer satisfaction (CSAT/NPS) – The borrower’s experience across the journey.

When these metrics move in the right direction, the LOS isn’t just saving time — it’s multiplying impact.

Implementation, Challenges, and ROI

Rolling out LOS isn’t about flipping a switch. It’s a project that needs ownership, training, and patience.

Start small — pilot one product line or region before going enterprise-wide. Clean your data, test integrations, and train your teams early. Most implementation issues come from old workflows or resistance to change, not the software itself.

The payoff comes quickly. Within weeks of going live, lenders see shorter loan cycles, fewer manual errors, and smoother audits. Operational costs dip because teams handle more applications with the same headcount.

ROI shows up both in numbers and experience. Faster disbursals and cleaner compliance improve borrower satisfaction; stronger credit evaluation cuts defaults. Together, those two outcomes justify the investment faster than most IT projects.

In short, the LOS return isn’t theoretical — it’s visible in your dashboards and your bottom line.

Why Finspectra PRIZM LOS Fits the Bill

Finspectra PRIZM LOS was built for lenders who outgrew spreadsheets but still need control. It combines flexibility with enterprise-grade compliance — the kind of system that can run across multiple branches without losing speed or consistency.

PRIZM’s modular setup means you can roll out what you need now and add more later. It’s AI-powered for better risk decisions, comes pre-aligned with RBI and CKYC norms, and connects seamlessly with credit bureaus, GSTN, and CRMs like HubSpot.

The interface feels intuitive — designed for lending teams, not developers — and deployments don’t drag for months. It’s fast, compliant, and scalable, making it a smart foundation for lenders ready to grow without chaos.

Conclusion

Lending has always been about balancing opportunity and risk. The right loan origination software makes that balance easier by giving teams structure, visibility, and confidence.

LOS isn’t just a tech upgrade; it’s the system that shapes how lenders grow. When workflows are clean, compliance is built-in, and data actually talks to each other, lending stops feeling manual and starts feeling intelligent.

For NBFCs, and fintechs, the takeaway is simple: a well-implemented LOS won’t replace your people; it’ll let them focus on smarter decisions, faster approvals, and better customer experiences.

And when that happens, lending isn’t a process anymore — it’s momentum.

FAQs

Q1: How does LOS shorten the loan cycle time?

By automating steps like KYC, credit scoring, and underwriting, LOS eliminates manual data handling. Approvals that once took days can now happen in hours — or minutes.

Q2: What’s the difference between LOS and LMS?

LOS handles everything before disbursal — application, credit checks, approvals. LMS manages what happens after disbursal — repayments, collections, and customer servicing.

Q3: Is LOS compliant with RBI and other lending regulations?

Yes, leading LOS platforms (like PRIZM) are built around compliance workflows. They log every step, enforce KYC/AML policies, and maintain audit trails.

Q4: How much does LOS cost?

Depending on deployment size, costs can range from a few lakhs annually (for smaller setups) to enterprise-scale investments. Cloud models usually have lower upfront costs than on-premise.

Q5: How does LOS help in credit risk assessment?

By using a mix of bureau data, alternate data, and rule-based scoring. AI-enhanced LOS platforms can even flag subtle risk indicators that traditional methods might miss.

.png)

.png)

.png)