%201.avif)

How Data Silos Are Slowing Credit Decisions and Delaying Loan Approvals

Credit teams rarely say, “We have a data silo problem.”

They say approvals are slow.

They say underwriting is overloaded.

They say SME files take too long to close.

But when you trace those delays backward, a common pattern emerges: fragmented borrower data across disconnected systems.

For banks, NBFCs, and fintech lenders, the real issue is not policy rigidity or risk appetite. It is decisioning friction. And most of that friction begins with how borrower data flows — or fails to flow — across the lending lifecycle.

This blog takes a decisioning-first look at data silos in lending, focusing specifically on how they slow credit assessments long before compliance risks or portfolio stress become visible.

What Data Silos Mean for Credit Decisioning

In theory, most lending environments are “integrated.” There is a CRM, a loan origination system, bureau connections, document management modules, core banking platforms, and servicing tools. APIs exist. Reports can be pulled. Dashboards are available.

But integration on paper is not the same as operational cohesion.

When borrower information is scattered across systems, the credit team does not experience a seamless flow of data. They experience fragmentation. Financial statements sit in one repository. Bureau outputs are stored elsewhere. Group exposure lives inside core systems. Servicing history may not even be visible during underwriting.

Instead of evaluating risk, analysts spend time reconstructing the borrower story.

Weak lending system integrations mean data must be searched, validated, and reconciled at multiple points in the loan approval process. Every reconciliation introduces pause. Every pause adds to turnaround time. And over hundreds or thousands of files, those minutes compound into systemic delays.

How Fragmented Data Slows Credit Decisions — Even Before Risk Is Assessed

Credit decisioning depends on clarity. Clarity about exposure. Clarity about cash flow. Clarity about borrower history.

When data is fragmented, clarity disappears.

Analysts often encounter multiple versions of the same borrower information — updated turnover figures in one system, revised loan structures in another, modified guarantor details somewhere else. Before underwriting can proceed, someone must confirm which data set is authoritative.

This verification work rarely appears in productivity metrics, but it materially extends the credit underwriting process.

The delay does not come from complex risk modeling. It comes from reconstructing inputs.

In many institutions, this invisible rework is the primary driver of underwriting delays. Analysts revisit financial summaries, revalidate exposure calculations, or request the same documents again simply because systems do not share a synchronized borrower view.

Over time, this creates a pattern of inconsistent approval timelines and escalating pressure from business teams asking why files are stuck.

Why SMEs Feel the Impact First

Fragmented data affects all loan types, but SME lending exposes the weakness faster.

Unlike salaried retail borrowers, SMEs present variable cash flows, layered ownership structures, related-party exposures, and sector-specific volatility. Risk assessment depends on contextual understanding rather than standardized income proofs.

When data gaps exist, the credit team cannot confidently interpret risk signals. A missing bank statement period, an outdated exposure figure, or an unsynced collateral value can materially alter a credit view.

As a result, analysts pause instead of proceeding.

This is why SME loan approvals often show disproportionate delays compared to similarly sized retail products. The sensitivity to data quality is higher, and the tolerance for inconsistency is lower.

If the question inside your organization is, “Why are SME credit decisions taking longer than expected?” the answer frequently lies in fragmented decisioning architecture rather than stricter underwriting.

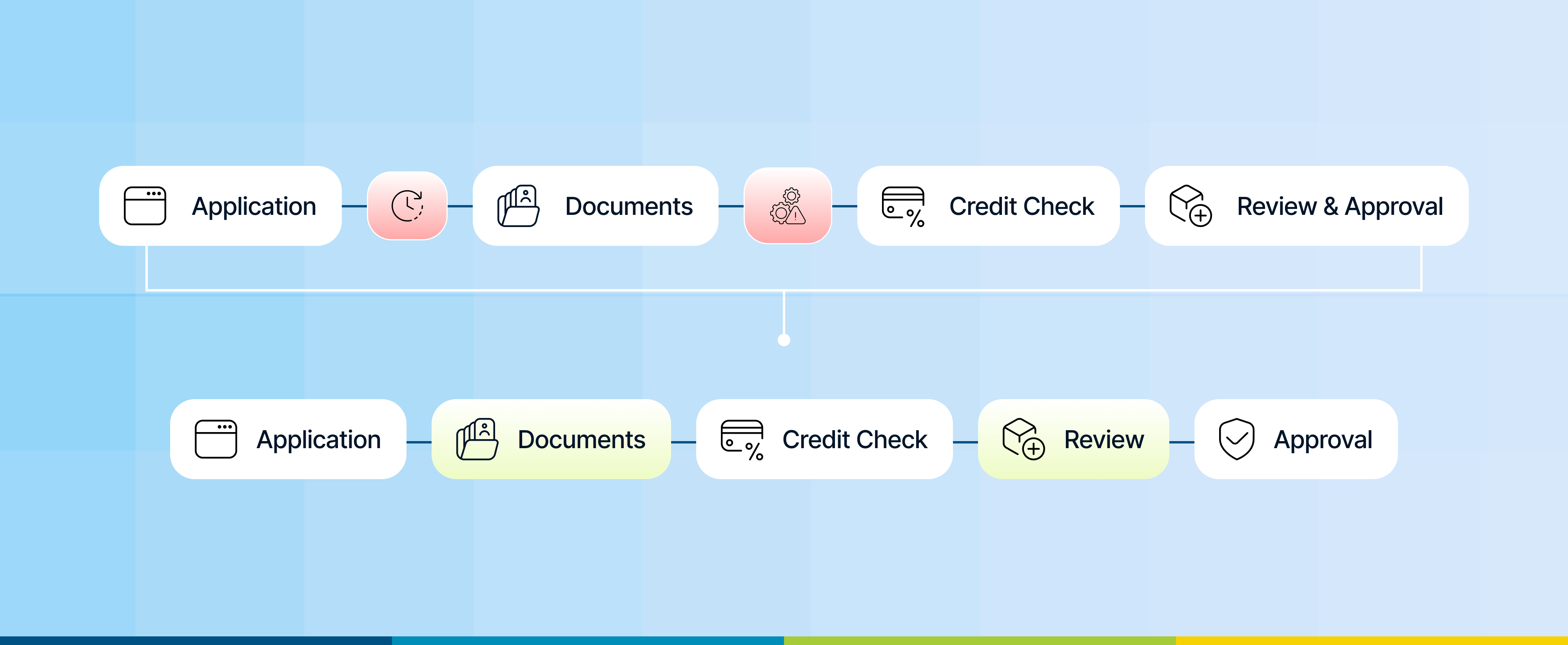

The Workflow Breakdown Behind Credit Decision Delays

In a typical fragmented setup, the sales team captures borrower details in one interface. Documents are uploaded through another. Bureau results are generated through an external connection. Exposure data sits inside core banking. Historical repayment behavior may be accessible only through servicing systems.

The credit analyst becomes the integration layer.

Instead of risk assessment being the primary cognitive task, navigation becomes the dominant activity. Screens are toggled. Reports are exported. Spreadsheets are created to reconcile discrepancies.

None of these actions improve risk insight. They simply compensate for disconnected systems.

This is where credit decision delays originate — not in risk policy, not in governance frameworks, but in broken workflow continuity.

By the time senior management notices longer approval cycles, the root cause is already embedded in daily operations.

Decisioning Impact Appears Before Portfolio Impact

Data silos are often discussed in the context of long-term consequences — higher NPAs, compliance risk, audit complexity. Those downstream effects are real and explored in detail in our blog The True Cost of Data Silos in Lending: NPAs, Delays, and Compliance Risks.

But from an operational standpoint, the earliest warning sign is slower decisioning.

Before risk quality deteriorates, speed deteriorates.

Files linger in underwriting queues. Clarification emails increase. Business teams escalate high-value cases. Approval timelines vary widely across similar borrower profiles.

These are not risk failures. They are architecture failures.

Can Credit Decision Speed Improve Without Replacing Everything?

This is the practical concern for most banks and NBFCs. Full system replacement is disruptive and capital-intensive. Yet living with fragmented workflows is equally costly in lost growth and competitive positioning.

The answer lies not in adding more point tools, but in strengthening borrower data continuity across systems.

Many lenders begin by modernizing their loan origination system to centralize underwriting inputs and enforce consistent data capture. Others enhance visibility through a connected loan servicing platform and exposure layers. Some adopt a more unified lending platform approach to reduce dependency on manual reconciliation while retaining core banking systems.

The key shift is conceptual: from “system ownership” to “borrower data ownership.”

When borrower data becomes centralized and accessible across the lifecycle — from origination to servicing — the credit team stops acting as a bridge between systems. Decisioning accelerates because visibility improves.

If you want to learn how leading lenders make this transition operationally, you can check our blog on From Fragmented to Unified: How Centralized Loan Management System Eliminates Data Silos.

The Competitive Implication of Slow Credit Decisions

In digital-first lending markets, speed is not just operational efficiency — it is competitive leverage.

SMEs compare approval timelines. Fintech lenders advertise rapid decisions. Relationship managers expect predictable turnaround times.

When internal data silos slow approvals, the borrower does not see architectural complexity. They see friction.

Over time, slow decisioning constrains growth more than risk appetite does. Opportunities are lost not because they were declined, but because they were delayed.

Closing Insight

Data silos in lending do not first manifest as rising defaults or audit observations. They first appear as hesitation inside underwriting.

As repeated clarification requests. As inconsistent approval timelines. As growing pressure from business teams.

If your institution is experiencing persistent loan approval delays, the issue may not lie in credit policy or analyst capacity. It may lie in how borrower data moves across your lending ecosystem. And decisioning speed improves only when that flow becomes seamless.

FAQs

1. Why do credit decisions take longer when borrower data is fragmented?

Because analysts must manually locate, validate, and reconcile borrower information across multiple systems before assessing risk. This reconstruction work extends the underwriting cycle even when risk criteria are straightforward.

2. How does incomplete data affect credit risk assessment for SMEs?

SME underwriting depends on contextual cash flow and exposure analysis. Missing or inconsistent inputs reduce confidence in risk interpretation, forcing analysts to delay approvals until clarity is restored.

3. What information do credit teams usually have to rework during loan approvals?

Common rework areas include financial statements, group exposure calculations, collateral values, updated borrower details, and bank statement summaries — especially when systems do not sync automatically.

4. Why are SME loan approvals more sensitive to data gaps than other loan types?

SMEs present variable income patterns and complex structures. Small inconsistencies in data can materially change risk evaluation, making underwriting more cautious and time-intensive.

5. Can lenders improve credit decision speed without replacing all existing systems?

Yes. By improving data continuity across systems, strengthening integrations, and centralizing borrower visibility, lenders can accelerate decisioning without a full technology overhaul.

.png)

.png)

.png)