%201.avif)

Is Your Lending Stack Holding You Back? A 10-Point Readiness Checklist for Modern Lenders

.png)

For many banks, NBFCs, and fintech lenders, growth no longer depends only on capital or distribution. It depends on the strength of the lending stack behind the scenes.

This is especially true for institutions offering lending software for businesses, where underwriting complexity and servicing scale demand stronger system architecture. If credit decisioning feels slow, integrations are fragile, or servicing costs keep rising, your lending technology may be the bottleneck.

This checklist is designed as a practical diagnostic tool. It will help you evaluate whether your current setup supports scalable, automated, and compliant modern lending — or whether it’s quietly holding you back.

What Is a Lending Stack in Digital Lending?

A lending stack is the complete set of systems that power your lending lifecycle — from origination to underwriting, disbursement, servicing, collections, and reporting.

It typically includes:

- Loan origination software

- Credit decisioning engines

- Loan management system

- Collections tools

- Reporting and analytics modules

- Lending system integrations with external data providers

In modern environments, these components operate as a unified end-to-end lending platform, not disconnected tools stitched together over time

The 10-Point Lending Stack Readiness Checklist

Use the questions below to evaluate where you stand.

1. Is Your Origination Flow Truly Digital and Automated?

If your loan origination software still requires manual data entry, document chasing, or email-based approvals, your growth will be constrained.

Operational consequence:

Manual processes increase turnaround time (TAT), reduce approval velocity, and introduce data errors that later affect servicing and compliance.

A modern lending stack should allow straight-through processing wherever risk policies permit.

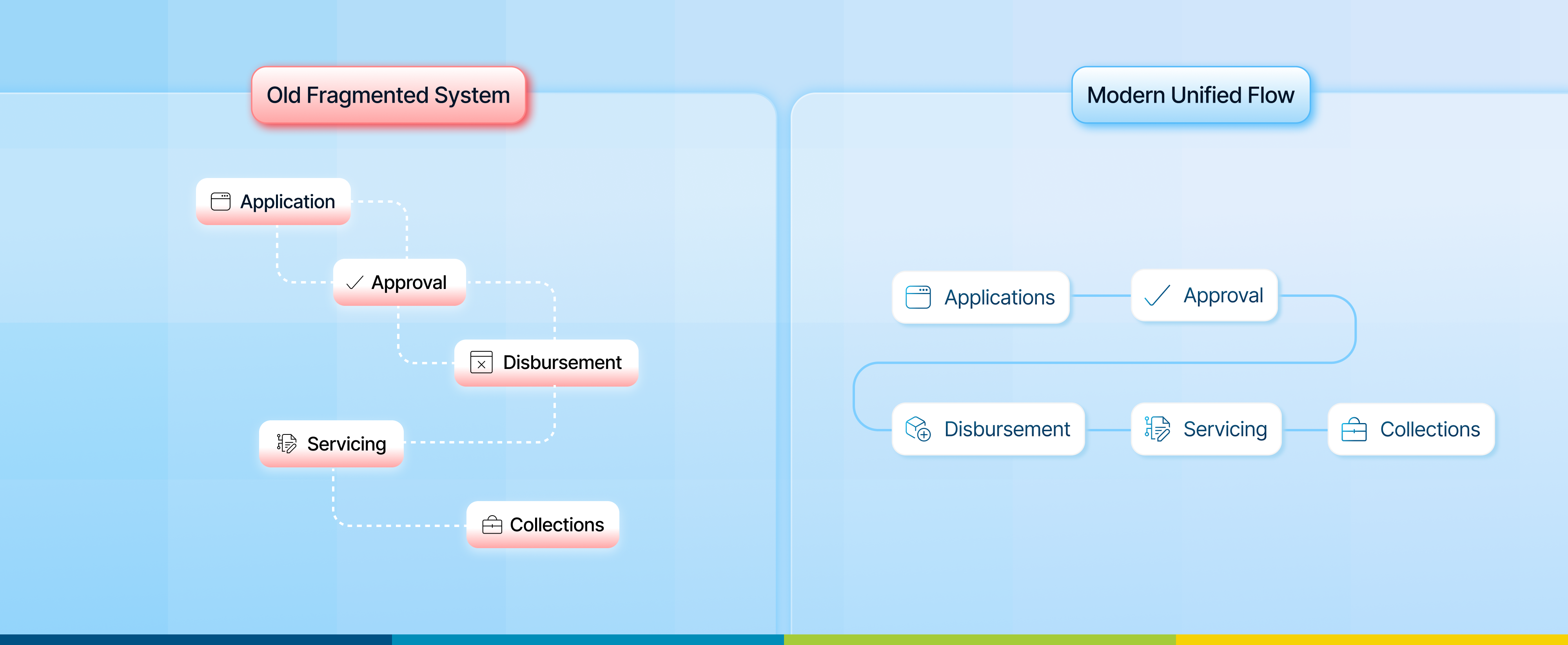

2. Are Your Systems Unified — or Patched Together?

Many lenders operate with separate systems for onboarding, underwriting, servicing, and collections.

If your team exports data between systems manually or relies heavily on APIs built years ago, your stack may be fragmented.

Operational consequence:

Fragmented systems create reconciliation issues, inconsistent borrower data, and reporting delays. This shift is one reason unified architectures are gaining traction — explored further in our blog — Why Unified Lending Platforms Are Replacing Patchwork Systems.

This is where an end-to-end lending platform can reduce complexity by centralizing workflows instead of relying on brittle integrations.

3. Can Your Lending Platform Scale Without Performance Drops?

Growth exposes weak architecture.

Ask yourself:

- Does approval time increase when application volumes rise?

- Do batch jobs fail during peak demand?

- Does your reporting lag during portfolio expansion?

Operational consequence:

If your lending platform cannot scale elastically, growth becomes operationally expensive and risky.

Scalable lending technology must support higher volumes without requiring proportional increases in headcount.

4. Is Credit Decisioning Configurable Without IT Dependency?

In modern lending, risk policies change frequently.

If every rule update requires development cycles, code changes, or vendor intervention, you are operating with rigidity.

Operational consequence:

Slow policy adjustments delay product launches and reduce competitiveness in fast-moving markets.

Modern digital lending solutions allow business users to configure rules and workflows without heavy IT reliance.

5. Does Your Loan Management System Support Automated Servicing?

Servicing inefficiencies often remain hidden until portfolios grow.

If your loan management system requires:

- Manual EMI adjustments

- Offline restructuring workflows

- Spreadsheet-based exception handling

you are accumulating operational risk.

Operational consequence:

Manual servicing drives higher cost per loan and increases compliance exposure.

Modern lending automation extends beyond origination into lifecycle servicing.

6. Are Your Collections Workflows Data-Driven?

Collections should not rely on static bucket strategies.

If your system cannot:

- Trigger automated reminders

- Segment borrowers dynamically

- Track recovery effectiveness in real time

..you are missing optimization opportunities.

Operational consequence:

Inefficient collections increase delinquency ratios and reduce portfolio yield.

Automation within the lending stack improves predictability and recovery outcomes.

7. Are Reporting and Compliance Real-Time or Reactive?

Regulatory reporting, audit trails, and portfolio analytics must be easily accessible.

If generating compliance reports requires data extraction and manual reconciliation, your risk posture is vulnerable.

Operational consequence:

Delayed or inconsistent reporting increases regulatory exposure and slows management decision-making.

A modern lending solution embeds audit logs and real-time dashboards into core workflows.

8. Do Your Integrations Limit Innovation?

Many lenders depend on external bureau checks, KYC providers, payment gateways, and analytics tools.

If adding a new partner requires lengthy integration cycles, your stack lacks flexibility.

Operational consequence:

Slow integrations delay product expansion and partnership strategies.

Well-architected lending system integrations allow modular expansion without disrupting core workflows.

9. Is Your Cost Per Loan Increasing as You Grow?

Scaling should reduce marginal cost per loan — not increase it.

If hiring operations staff is your primary growth strategy, automation gaps likely exist.

Operational consequence:

Higher operating costs compress margins, particularly in competitive lending markets.

This is often where modern lending automation delivers measurable financial impact.

10. Can You Launch a New Lending Product in Weeks — Not Months?

Product agility is a key test of readiness.

If launching a new product requires:

- Core code rewrites

- Manual workarounds

- Separate workflows

your stack is limiting innovation.

Operational consequence:

Slow product rollout reduces competitive advantage and market responsiveness.

Modern lending platforms are designed for configurable product templates and rapid deployment.

When Should Lenders Modernize Their Lending Stack?

Modernization becomes urgent when:

- Approval TAT continues to increase despite process reviews

- Operational costs rise faster than portfolio growth

- Compliance complexity outpaces system capabilities

- Product launches consistently miss timelines

- Technology teams spend more time maintaining legacy tools than building new capabilities

Modernization is not about replacing everything at once. It is about moving toward a cohesive architecture that supports automation, scalability, and configurability.

Final Self-Assessment

If you answered “no” to more than three checklist items, your lending stack may be acting as a growth constraint rather than an enabler.

Modern lending demands:

- Unified workflows

- Automated lifecycle management

- Scalable architecture

- Flexible configuration

- Real-time visibility

The question is not whether modernization will eventually be required — but whether your current lending stack is already slowing you down.

FAQs

1. What is a lending stack in digital lending?

A lending stack is the full technology ecosystem that supports loan origination, underwriting, disbursement, servicing, collections, and reporting within a digital lending operation.

2. How do I know if my lending software is outdated?

Common indicators include heavy manual intervention, slow integrations, limited configurability, and performance issues during high application volumes.

3. What are common signs a lending stack doesn’t scale well?

Rising cost per loan, system slowdowns during peak traffic, increased error rates, and frequent reconciliation issues are strong signals of poor scalability.

4. Why does lending automation matter for growth?

Lending automation reduces manual effort, lowers operational costs, shortens turnaround times, and improves borrower experience — all of which directly impact growth and portfolio quality.

5. When should lenders modernize their lending stack?

Modernization should be considered when operational inefficiencies begin limiting expansion, compliance risks increase, or product innovation slows due to technology constraints.

.png)

.png)

.png)