%201.avif)

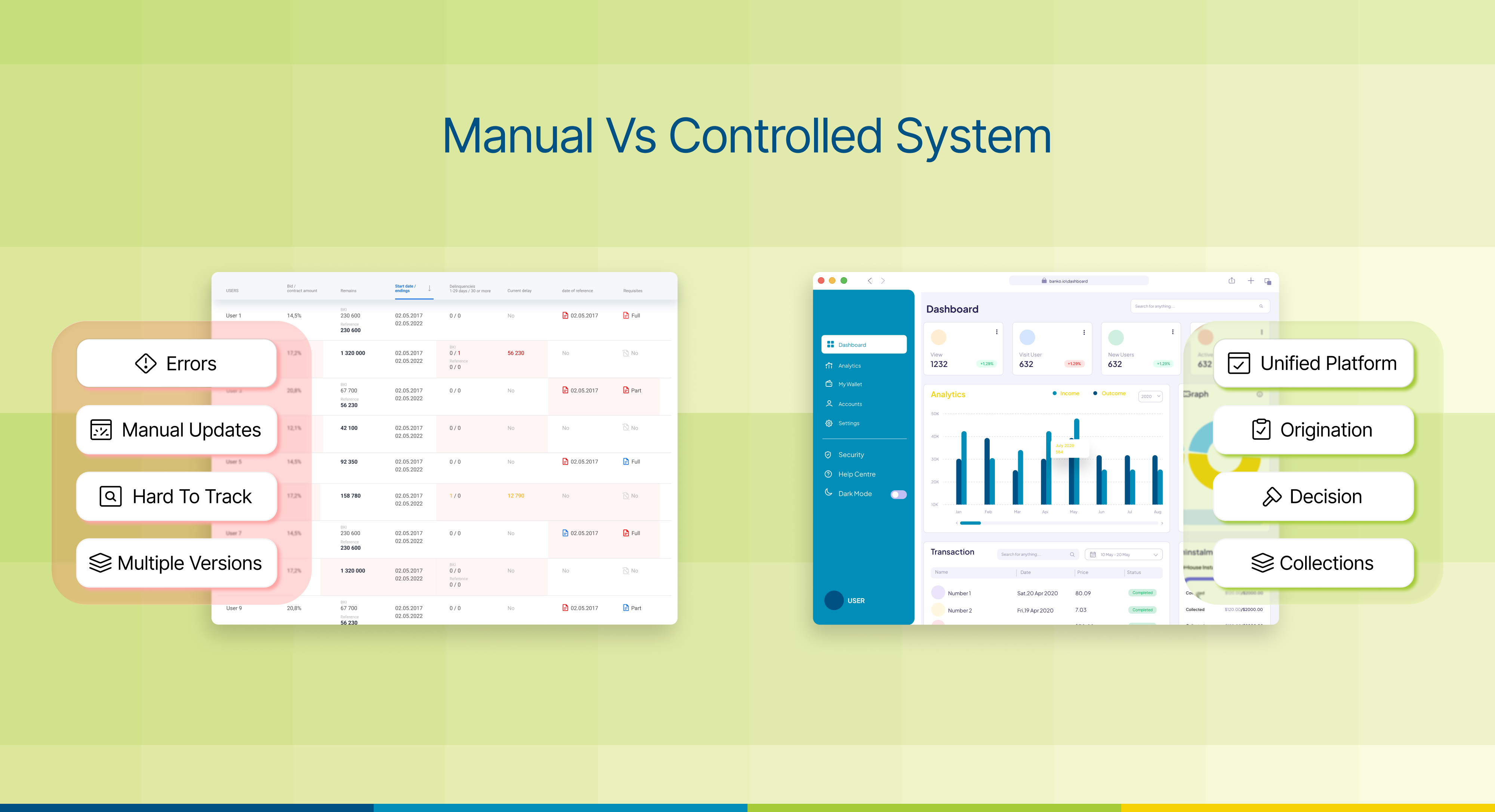

The Compliance Risks of Spreadsheet-Based Loan Management

.png)

For many lenders, spreadsheet-based loan management does not begin as a strategic choice. It emerges gradually.

A spreadsheet created to track a handful of loans becomes the operating system for a growing portfolio. Additional tabs are added. New formulas are introduced. Teams begin sharing versions by email. Before long, critical lending decisions, regulatory reports, repayment schedules, and compliance records depend on files that were never designed to support institutional-scale operations.

The problem is not that spreadsheets are inherently flawed. They remain useful analytical tools. The challenge begins when spreadsheet-based loan management evolves from a supporting function into the primary system of record.

At that point, compliance risk becomes a structural issue rather than an operational inconvenience.

As regulatory expectations around data integrity, auditability, customer protection, and reporting continue to rise, lenders face a difficult reality: a process that appears manageable on the surface may contain significant hidden vulnerabilities underneath.

This article examines the compliance risks associated with spreadsheet-based loan management, why regulators increasingly expect stronger controls, and how lenders can build more resilient operating environments without disrupting business growth.

Why Spreadsheet-Based Loan Management Persists

Despite the availability of sophisticated lending platforms, spreadsheets continue to play a central role across many lending organizations, particularly among growing NBFCs and specialty finance institutions.

The reasons are understandable. Spreadsheets are familiar, inexpensive, and highly flexible. Teams can create custom calculations, adapt workflows quickly, and avoid lengthy implementation projects.

In the early stages of growth, these advantages often outweigh the drawbacks.

The challenge emerges as lending operations become more complex. Regulatory obligations increase. Portfolio sizes expand. Multiple teams require access to the same information. External auditors request evidence trails. Regulators expect consistent reporting across business functions.

What once felt agile begins to create friction.

A process that relies heavily on manual intervention often struggles to deliver the consistency and traceability that modern compliance frameworks require.

Compliance Is No Longer Just About Following Rules

A significant shift has occurred in regulatory thinking over the past decade.

Historically, compliance reviews focused largely on outcomes. Regulators wanted to know whether calculations were correct, reports were filed, and policies were followed.

Today, regulators increasingly want to understand the process behind those outcomes.

They want to know where data originated, who modified it, when changes occurred, and whether sufficient controls existed throughout the lifecycle of that information.

This distinction matters because a lender may produce an accurate report while still failing to demonstrate how that report was generated.

That gap creates compliance exposure.

The growing emphasis on data governance, audit trails, and operational transparency reflects a broader industry recognition that reporting accuracy is only as reliable as the processes supporting it.

The Audit Trail Problem

Alt text for the image: Spreadsheet-based loan management audit trail breakdown showing fragmented files versus centralized compliance tracking system flow

One of the most significant compliance risks associated with spreadsheet-based loan management is the absence of a dependable audit trail.

Every regulated lending institution eventually faces scrutiny from auditors, regulators, internal control teams, or risk committees. During these reviews, evidence becomes just as important as outcomes.

A spreadsheet can show the current state of information. It often struggles to show the complete history behind that information.

Consider a loan restructuring approved six months ago. An auditor may ask:

- Who modified the repayment schedule?

- When was the change made?

- What approval supported the modification?

- Was the previous version retained?

Answering these questions can become surprisingly difficult when records are maintained across multiple spreadsheet versions.

According to principles established under BCBS 239, financial institutions are expected to maintain accurate, complete, and traceable risk data. While originally developed for globally significant banks, these principles increasingly influence broader expectations around governance and reporting across the lending sector.

Without a reliable audit trail, organizations often find themselves reconstructing events after the fact. That process is time-consuming, expensive, and vulnerable to error.

Human Error Becomes a Compliance Event

Most discussions about spreadsheets focus on operational inefficiency. The larger issue is that seemingly minor errors can quickly become compliance concerns.

A misplaced decimal point, overwritten formula, incorrect interest calculation, or accidental data deletion may appear trivial in isolation.

In a lending environment, each of these mistakes can affect customer disclosures, regulatory reporting, collections activity, or portfolio performance calculations.

Recent industry surveys have found that loan calculation discrepancies remain a recurring challenge for lenders, with many organizations reporting errors on a monthly or even weekly basis.

The underlying issue is not employee capability.

It is system design.

When critical processes depend on repetitive manual actions, error rates become a function of volume rather than competence.

The scale of this challenge is evident across the lending industry. A 2025 survey of more than 2,000 lending, banking, auto finance, and fintech professionals found that over two-thirds of organizations experience loan payment discrepancies on a weekly or monthly basis. Nearly half said compliance issues such as inaccurate APRs or outdated disclosures had already resulted in rework, audit findings, or legal exposure.

As portfolios grow, the probability of mistakes increases. Compliance teams are then forced into a reactive cycle of identifying, investigating, and correcting issues that could have been prevented through stronger controls.

Version Control Creates Invisible Risk

Few compliance risks receive less attention than version control.

Most organizations have experienced some variation of the same scenario. Multiple teams access the same spreadsheet. Copies are downloaded locally. Updates occur independently. Several versions begin circulating simultaneously.

Eventually, nobody can say with certainty which version is authoritative.

The consequences extend beyond operational confusion.

When different teams work from inconsistent data sets, lenders risk generating conflicting reports, applying outdated information to customer accounts, and producing records that cannot be reconciled during audits.

Compliance failures are often associated with major events. In practice, many originate from small inconsistencies that accumulate over time.

Version fragmentation is one of the most common examples.

The absence of a single source of truth introduces uncertainty into every downstream process that relies on that data. This fragmentation is not just a spreadsheet issue, it is part of a wider structural problem in lending operations where data silos increase reconciliation effort, reporting delays, and compliance risk across the institution.

Regulatory Change Is Difficult to Operationalize in Spreadsheets

Regulation rarely stands still.

Consumer protection requirements evolve. Reporting standards change. Disclosure obligations expand. Data privacy frameworks continue to mature across jurisdictions.

For lenders operating through spreadsheet-based loan management, every regulatory update creates a manual implementation exercise.

Formulas must be reviewed.

Templates require modification.

Validation checks need updating.

Staff must verify that new calculations are being applied consistently across every active spreadsheet.

This creates a dependency on institutional memory rather than systematic controls.

The risk is not simply that a change will be missed. Regulatory change management is already a significant challenge for lenders. In the same 2025 industry survey, 60% of lenders reported struggling to keep pace with changing regulations. For organizations relying on spreadsheet-driven workflows, every regulatory update often requires manual revisions, testing, and validation across multiple files, increasing the likelihood of inconsistencies.

The risk is that some teams will implement it while others continue using older versions, resulting in inconsistent compliance practices across the organization.

Regulatory compliance becomes increasingly difficult when control mechanisms exist primarily within individual files rather than centralized systems.

This challenge is exactly why lenders are increasingly moving toward structured platforms, as discussed in how modern systems simplify regulatory compliance for lenders without relying on fragmented spreadsheet workflows.

Access Control and Data Security Concerns

Compliance extends beyond calculations and reporting.

It also encompasses how customer information is protected.

Loan records contain sensitive financial data, personal identifiers, repayment histories, and credit information. Regulators increasingly expect organizations to demonstrate robust controls over who can access that information and how it is used.

Spreadsheets provide only limited support for sophisticated permission structures.

Files are frequently shared through email, downloaded onto local devices, or stored across multiple locations.

As organizations grow, maintaining consistent access controls becomes increasingly difficult.

This creates two separate risks.

The first is unauthorized access.

The second is the inability to demonstrate appropriate governance when questions arise later.

Both can create significant compliance exposure.

What Happens When an NBFC Fails a Compliance Audit?

Compliance audits rarely fail because of a single catastrophic event.

More often, auditors identify recurring weaknesses that indicate broader control deficiencies.

These may include incomplete documentation, inconsistent records, inadequate approval workflows, poor change management practices, or insufficient evidence supporting reported figures.

The direct consequences vary by jurisdiction and regulatory framework.

However, common outcomes include remediation requirements, heightened regulatory scrutiny, operational disruption, additional reporting obligations, and increased compliance costs.

The indirect consequences are often more significant.

Management attention shifts away from growth initiatives.

Resources are redirected toward corrective action.

Stakeholder confidence can weaken.

The longer these issues persist, the more difficult they become to address.

Spreadsheet-Based Loan Management vs Loan Management Software

Why Lenders Are Moving Toward Purpose-Built Systems

The case for modern loan management software is not primarily about efficiency.

It is about control.

As lending operations become more regulated, organizations need systems that embed governance directly into daily workflows.

A modern web based loan management system provides structured audit trails, role-based permissions, workflow controls, automated reporting, and centralized data management.

These capabilities reduce dependence on manual intervention while improving transparency across the loan lifecycle.

For growing lenders, the shift is increasingly viewed as a compliance decision rather than a technology decision. Platforms such as the Prizm Lending Suite are designed to replace fragmented spreadsheet-based loan management with a unified system that embeds auditability, controls, and workflow governance into daily lending operations.

Similarly, NBFC compliance software is being adopted not simply to satisfy regulatory requirements but to create operational environments where compliance becomes easier to demonstrate and maintain.

The objective is not to eliminate human oversight.

It is to ensure that oversight occurs within a controlled framework.

Conclusion

Spreadsheets remain valuable tools for analysis, forecasting, and ad hoc reporting. Problems arise when they become the foundation of regulated lending operations.

The compliance risks associated with spreadsheet-based loan management are rarely visible in day-to-day activities. They emerge during audits, regulatory reviews, customer disputes, and periods of rapid growth. By that stage, remediation is often far more expensive than prevention.

The question facing lenders today is not whether spreadsheets can support loan operations. Many already do.

The more important question is whether those processes can withstand the scrutiny that accompanies growth, regulation, and increasing stakeholder expectations.

As compliance requirements continue to evolve, lenders that invest in stronger controls, better auditability, and purpose-built systems will be better positioned to scale with confidence.

If your organization is evaluating ways to reduce the risks of manual loan processing and strengthen compliance readiness, explore how FinSpectra’s loan management platform helps lenders create transparent, audit-ready operations built for long-term growth.

FAQs

Are spreadsheets compliant for loan management?

Spreadsheets are not inherently non-compliant, but they can create compliance challenges when used as the primary system for managing loan portfolios. As lending operations grow, spreadsheets often lack the audit trails, access controls, version management, and data governance capabilities regulators and auditors expect. Compliance depends not only on the accuracy of information but also on an institution’s ability to demonstrate how that information was created, modified, and approved.

What is an audit trail in loan management?

An audit trail is a chronological record of actions performed throughout the loan lifecycle. It captures details such as who accessed a loan record, what changes were made, when those changes occurred, and whether the changes were approved. Audit trails help lenders demonstrate accountability, support internal investigations, and provide evidence during regulatory reviews and compliance audits.

What happens if an NBFC fails a compliance audit?

The consequences depend on the nature and severity of the findings. An NBFC may be required to implement corrective actions, strengthen internal controls, submit additional reports, or undergo enhanced regulatory scrutiny. Compliance failures can also increase operational costs, consume management bandwidth, delay growth initiatives, and affect stakeholder confidence.

How can lenders replace spreadsheets safely?

The most effective approach is a phased transition rather than a complete overhaul. Lenders should first identify critical processes that present the highest compliance risk, such as loan servicing, repayment tracking, and regulatory reporting. Implementing a loan management software platform alongside existing workflows allows teams to validate data, train users, and migrate operations gradually while maintaining business continuity.

What are the biggest spreadsheet risks in lending?

The most significant risks include limited auditability, manual data-entry errors, version-control issues, inconsistent calculations, weak access controls, and difficulties adapting to regulatory changes. These challenges can lead to inaccurate reporting, compliance breaches, audit observations, and operational inefficiencies, particularly as loan portfolios become larger and more complex.

.png)

.png)