%201.avif)

Top Digital Lending Challenges in MSME Financing and How Fintechs Are Addressing Them

.png)

Micro, small, and medium enterprises (MSMEs) are the backbone of economies worldwide. They drive employment, support innovation, and contribute significantly to GDP across both developed and emerging markets. Yet despite their economic importance, access to formal credit remains one of the most persistent barriers to growth.

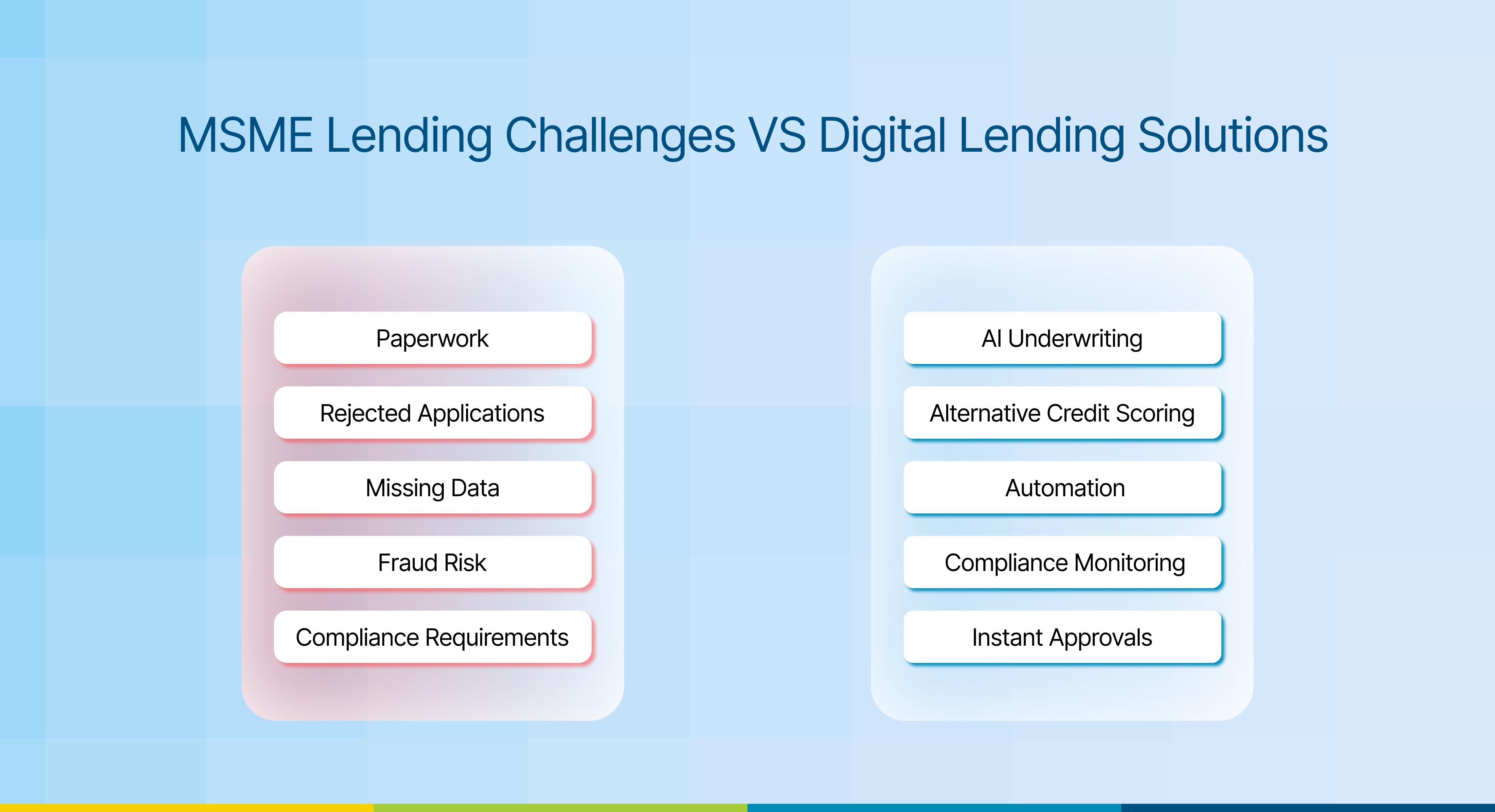

Many of the lending challenges in MSME financing are well known. Small businesses often lack extensive credit histories, standardized financial records, or collateral that traditional lenders rely on during underwriting. At the same time, lenders face increasing pressure to reduce costs, accelerate approvals, strengthen risk controls, and comply with evolving regulations.

The scale of the problem is substantial. According to the International Finance Corporation (IFC), the global MSME finance gap stands at approximately $5.7 trillion, highlighting the continued mismatch between credit demand and credit availability.

Digital lending has emerged as a powerful response to this challenge. However, technology alone does not solve structural issues in small business lending. The lenders making meaningful progress are those using digital capabilities to improve underwriting quality, operational efficiency, compliance, and portfolio performance simultaneously.

This article examines the most significant lending challenges in MSME financing and explores how fintech lending solutions are helping financial institutions address them.

Why MSME Financing Remains a Global Challenge

For decades, MSME lending has presented a difficult equation for banks and non-bank lenders. Small businesses often require modest loan amounts, yet evaluating those applications can involve nearly the same effort as underwriting larger corporate borrowers.

The result is a market where demand for credit continues to outpace supply.

The challenge extends beyond individual businesses. According to the Asian Development Bank, the global trade finance gap remained at $2.5 trillion in 2025, representing roughly 10% of global trade. Small and medium-sized enterprises continue to account for a significant share of unmet financing demand.

Digital technologies have improved access and efficiency, but lenders still face fundamental questions around risk assessment, data quality, compliance, fraud prevention, and profitability. These realities define today’s lending challenges in MSME financing.

For a broader perspective on how digital lending models are evolving across sectors, explore our guide to digital lending solutions across industries.

Limited Credit Histories and Outdated Underwriting Models

One of the most common lending challenges in MSME financing is the inability to evaluate borrowers through traditional credit frameworks.

Many small businesses operate successfully while maintaining limited borrowing histories. Others may have strong revenues but lack audited financial statements or substantial collateral. Conventional underwriting models often struggle to assess these businesses accurately.

The problem is not necessarily a lack of creditworthiness. More often, it is a lack of visibility.

This is where alternative credit scoring is changing the lending landscape. Rather than relying solely on bureau data and financial statements, lenders increasingly evaluate cash flow patterns, bank transactions, tax filings, accounting software data, payment histories, and marketplace activity.

The objective is not to replace traditional risk assessment. It is to create a more complete picture of business performance and repayment capacity.

As digital ecosystems expand, alternative credit scoring is helping lenders reach previously underserved segments while maintaining stronger risk discipline.

High Origination Costs Continue to Limit MSME Lending

The economics of MSME lending have historically been difficult.

Many lenders still operate processes built around manual document collection, repetitive verification steps, fragmented workflows, and multiple approval layers. These inefficiencies increase acquisition costs and reduce profitability, particularly for smaller loan values.

This remains one of the most significant lending challenges in MSME financing because operational costs directly influence a lender’s ability to serve smaller businesses at scale.

Fintech lending solutions are addressing this challenge through automation.

Digital onboarding, automated document verification, workflow orchestration, electronic signatures, and straight-through processing reduce manual effort across the lending lifecycle. What previously required days or weeks can often be completed within hours.

The impact extends beyond faster approvals. Lower operating costs enable lenders to serve more borrowers while improving portfolio economics.

Data Gaps and Information Asymmetry

Lenders make decisions based on information. When information is incomplete, uncertainty increases.

Many MSMEs still operate across fragmented systems. Financial records may be spread across spreadsheets, accounting applications, payment platforms, and banking relationships. Some businesses maintain limited historical records altogether.

These challenges often stem from fragmented data environments, a problem explored in greater detail in our article on the true cost of data silos in lending.

This creates information asymmetry between borrowers and lenders, making accurate risk assessment more difficult.

Addressing this issue has become a priority across the digital lending industry.

Modern digital lending platform ecosystems increasingly leverage open banking frameworks, API integrations, account aggregation models, ERP connectivity, and real-time financial data sources. These capabilities provide lenders with deeper visibility into business operations and cash flow behaviour.

The result is more informed underwriting and stronger credit decisions.

For lenders seeking sustainable portfolio growth, solving data fragmentation has become central to overcoming lending challenges in MSME financing.

Navigating a More Complex Regulatory Environment

Digital lending has expanded rapidly, but regulatory expectations have evolved just as quickly.

Across markets, regulators are increasing their focus on transparency, consumer protection, data privacy, algorithmic accountability, and third-party risk management. Lenders are expected to demonstrate not only compliance but also governance over increasingly digital processes.

In India, the RBI digital lending guidelines have become a significant reference point for responsible digital lending practices. Similar regulatory developments are emerging across multiple jurisdictions as policymakers seek greater oversight of digital credit ecosystems.

Compliance can no longer be treated as a separate function operating alongside lending operations. It must be embedded directly into workflows, decision engines, and customer journeys.

We discuss this shift in detail in our guide on how loan management software simplifies regulatory compliance for lenders.

Many fintech lending solutions now incorporate automated compliance checks, consent management frameworks, audit trails, policy controls, and reporting capabilities that help institutions manage regulatory obligations more effectively.

For lenders operating across multiple products or geographies, compliance infrastructure is increasingly becoming a strategic capability rather than a regulatory necessity.

Managing Fraud Without Creating Customer Friction

The shift toward digital channels has improved convenience for borrowers, but it has also expanded opportunities for fraud.

Identity manipulation, document forgery, synthetic identities, account takeover attempts, and application fraud continue to challenge lenders worldwide.

The difficulty lies in balancing security with customer experience.

Lengthy verification processes may reduce fraud exposure, but they can also increase abandonment rates and slow down approvals. Excessive friction undermines one of the primary advantages of MSME digital lending.

As a result, many lenders are investing in advanced fraud detection capabilities that operate in real time. Machine learning models, behavioural analytics, device intelligence, biometric verification, and continuous monitoring help institutions identify suspicious activity without disrupting legitimate borrowers.

The most effective fraud strategies focus on precision rather than additional process layers.

Balancing Speed with Credit Quality

Borrowers increasingly expect near-instant decisions.

Yet many institutions continue to struggle with approval bottlenecks, a challenge we examine in our article on why loan approvals still take days and what lenders can do differently.

Digital experiences offered by leading consumer platforms have reshaped expectations across financial services. MSME borrowers now expect similar convenience when applying for business credit.

However, faster decisions do not automatically lead to better lending outcomes.

One of the enduring lending challenges in MSME financing is balancing speed with prudent risk management. Rapid approvals are valuable only when underwriting quality remains intact.

Leading fintech lenders are moving beyond static credit models toward dynamic risk assessment. Instead of evaluating borrowers at a single point in time, they continuously monitor performance indicators throughout the customer lifecycle.

This shift allows lenders to identify emerging risks earlier while supporting faster credit decisions.

The future of fintech lending will depend not on how quickly loans are approved, but on how effectively lenders manage risk after disbursement.

Meeting Diverse Working Capital Needs

Not all MSMEs require traditional term loans.

Many businesses need short-term liquidity linked to inventory cycles, supplier payments, receivables, seasonal demand fluctuations, or purchase orders. Traditional loan structures often fail to address these requirements effectively.

This creates another layer of lending challenges in MSME financing.

Fintech innovation has expanded the range of available credit products. Invoice financing, embedded lending, revenue-based financing, supply chain finance, and marketplace-based lending models are helping businesses access capital that aligns more closely with operational realities.

Data-driven underwriting allows lenders to assess these financing opportunities using actual business activity rather than relying solely on historical financial statements.

As MSME financing continues to evolve, flexibility will become as important as access.

The Technology Shaping the Future of MSME Lending

The next phase of MSME lending will not be defined by a single technology. It will be shaped by the convergence of data, automation, intelligence, and connectivity.

Alternative credit scoring is improving visibility into borrower performance. Artificial intelligence is helping lenders evaluate applications more efficiently. Open banking frameworks are expanding access to financial data. Embedded finance is bringing credit closer to the point of need. Automation is reducing operational complexity across the lending lifecycle.

Together, these capabilities are transforming how lenders approach lending challenges in MSME financing.

What once required extensive manual intervention can increasingly be executed through integrated digital workflows that improve both efficiency and risk management.

How Modern Lending Platforms Help Lenders Scale MSME Financing

Technology adoption alone does not solve lending challenges in MSME financing. The real value comes from connecting underwriting, compliance, servicing, collections, and portfolio monitoring within a unified operating model.

This is one reason many lenders are moving away from disconnected technology stacks, as discussed in our article on why unified lending platforms are replacing patchwork systems.

A modern digital lending platform enables lenders to automate origination, standardize credit processes, strengthen governance, and gain greater visibility across the entire loan lifecycle.

For banks, NBFCs, and fintech lenders, this creates the foundation for scalable MSME financing.

For a closer look at how technology supports commercial and small-business lending operations, read our guide to business lending software.

As competition intensifies and regulatory expectations continue to rise, institutions will need platforms that support both growth and control. The ability to make faster decisions, manage risk effectively, and deliver consistent borrower experiences will increasingly determine long-term success.

Final Thoughts

The discussion around MSME financing often focuses on access to credit. While access remains important, the larger challenge is creating lending models that are sustainable for both borrowers and lenders.

The most pressing lending challenges in MSME financing are no longer limited to credit availability. They include data quality, underwriting accuracy, operational efficiency, fraud prevention, regulatory compliance, and portfolio resilience.

Fintech innovation is helping address many of these issues, but success depends on how technology is applied across the lending value chain.

The institutions that will lead the next phase of MSME lending are unlikely to be those that simply digitize existing processes. They will be the ones that use technology to make better credit decisions, operate more efficiently, and build stronger relationships with the businesses they serve.

.png)

.png)